SIFA App 2

Appendix B: Own funds - worked examples

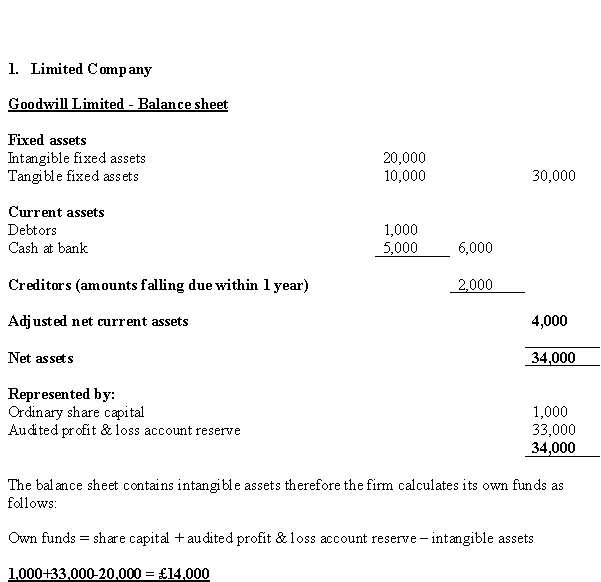

SIFA App 2.1

Appendix B: Own funds - worked examples

- 09/09/2005

SIFA App 2.1.1

See Notes

- 09/09/2005

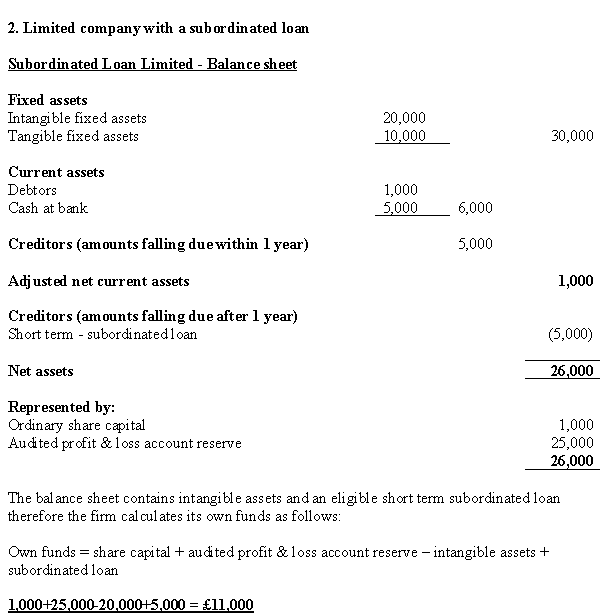

SIFA App 2.1.2

See Notes

- 09/09/2005

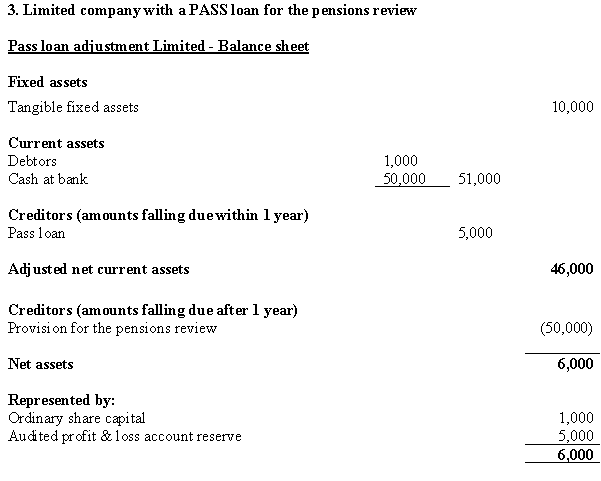

SIFA App 2.1.3

See Notes

| The firm applied for and was granted a PASS loan facility of £55,000 in January 2000 at that time the firm made a provision for pension review redress of £60,000. The firm has drawn down £6,000 of the facility and subsequently repaid £1000. |

| The Pass loan adjustment = lower of the agreed loan facility less repayments £54,000 (£55,000 -£1000) & provision at the time of applying for the Pass loan facility £60,000. |

| Own funds = share capital + audited profit & loss account reserve + Pass loan adjustment |

| 1,000+5,000+54,000 = £60,000 |

- 09/09/2005

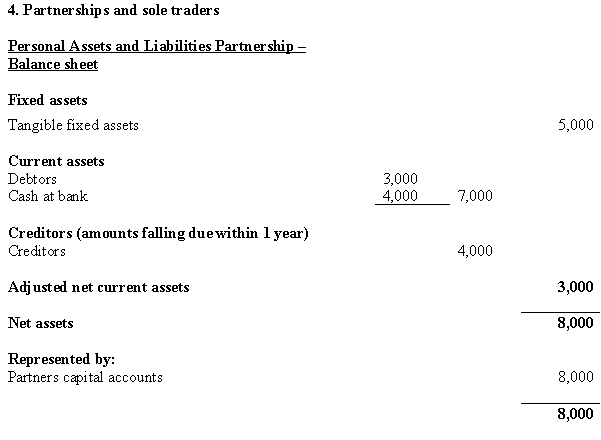

SIFA App 2.1.4

See Notes

| In addition the Partners have combined personal assets of £100,000 and personal liabilities of £20,000. |

| Own funds = Partners capital accounts + to the extent necessary to make up any shortfall in the required resources Personal assets - Personal liabilities |

| 8,000+2,000 = £10,000 |

| £2,000 is the amount of personal assets required to make up the shortfall in the required resources. The firm's partners have £80,000 in net personal assets but are only required to contribute £2,000 for the calculation. |

| The calculation for sole traders is exactly the same as the one above. In addition if the firm had: •Intangible assets these would need to be deducted in the same way as in example 1.•Subordinated loans these can be added as in example 2.•Pass loans then these can be adjusted as in example 3.

|

- 09/09/2005