MIGI 14

Complaints

MIGI 14.1

Introduction

- 01/12/2004

MIGI 14.1.1

See Notes

- 31/05/2005

MIGI 14.2

How to handle a complaint

- 01/12/2004

MIGI 14.2.1

See Notes

- 01/12/2004

MIGI 14.2.2

See Notes

- 31/05/2005

MIGI 14.2.3

See Notes

- 01/12/2004

MIGI 14.2.4

See Notes

- 01/12/2004

Where and when should you publicise your procedures?

MIGI 14.2.5

See Notes

- 31/05/2005

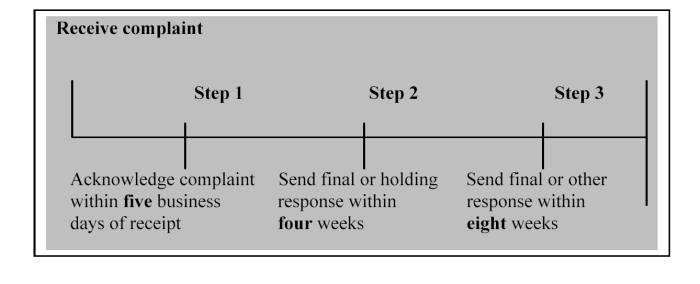

How quickly do you need to deal with a complaint?

MIGI 14.2.6

See Notes

- 01/12/2004

MIGI 14.2.7

See Notes

- 01/12/2004

Where are the relevant Handbook sections?

MIGI 14.2.8

See Notes

- 31/05/2005

Complaints about matters that occurred prior to the commencement of regulation

MIGI 14.2.9

See Notes

- 31/05/2005

Record keeping requirements

MIGI 14.2.10

See Notes

- 31/05/2005

MIGI 14.3

Complaints reporting to the FSA

- 01/12/2004

MIGI 14.3.1

See Notes

- 01/12/2004

When and how often should I submit complaints reports?

MIGI 14.3.2

See Notes

- 31/05/2005

MIGI 14.3.3

See Notes

- 31/05/2005

How do I submit a report?

MIGI 14.3.4

See Notes

- 31/05/2005

MIGI 14.3.5

See Notes

| Reporting Requirements - Part I, Chapter 11.1 |

| The FCSC and The FOS - Part I, Chapter 18 |

- 01/12/2004