MIGI 11

Reporting and Notifications

MIGI 11.1

Reporting requirements

- 01/12/2004

MIGI 11.1.1

See Notes

- 01/12/2004

Why do we require periodic information from firms?

MIGI 11.1.2

See Notes

- 01/12/2004

How is information submitted?

MIGI 11.1.3

See Notes

- 01/12/2004

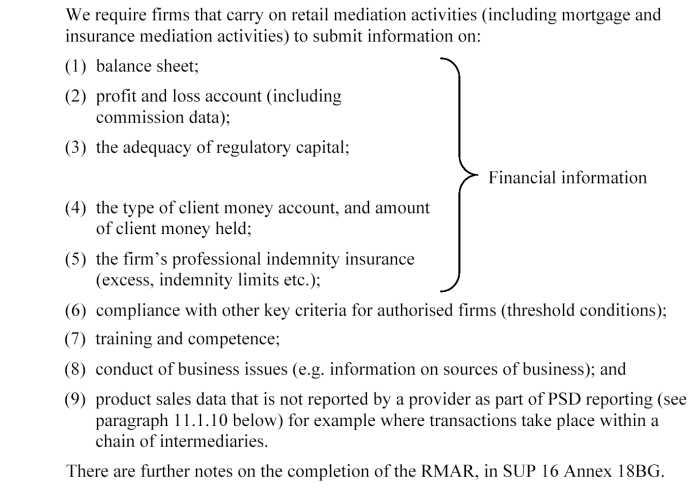

What information do you need to submit in the RMAR?

MIGI 11.1.4

See Notes

- 01/12/2004

When and how often do I have to submit the RMAR?

MIGI 11.1.5

See Notes

- 01/12/2004

MIGI 11.1.6

See Notes

- 01/12/2004

MIGI 11.1.7

See Notes

- 01/12/2004

MIGI 11.1.8

See Notes

- 01/12/2004

Other reporting requirements

MIGI 11.1.9

See Notes

- 01/12/2004

MIGI 11.1.10

See Notes

- 01/12/2004

MIGI 11.2

Notifications

- 01/12/2004

MIGI 11.2.1

See Notes

- 01/12/2004

Matters having a serious regulatory impact

MIGI 11.2.2

See Notes

- 01/12/2004

Communications with us in line with Principle 11

MIGI 11.2.3

See Notes

| 1. Any proposed restructuring, reorganisation or business expansion, which could have a significant impact on your firm's risk profile or resources, including but not limited to: | |

| Starting to provide a new product or service (you may need to apply for a variation of permission). | |

| Ceasing to undertake a regulated or ancillary activity, or significantly reducing the scope of such activities. (You may need to apply for a variation of permission). | |

| Entering into, or significantly changing, a material outsourcing arrangement. | |

| Any change in your firm's prudential category. | |

| 2. Any significant failure of your firm's systems or controls (including those reported to your firm by your auditor - if applicable). | |

| 3. Any action that your firm proposes to take which would result in a material change in its capital adequacy or solvency including, but not limited to: | |

| Any action that would result in a material change in your firm's financial resources or financial resources requirement. | |

| A material change resulting from the payment of a special or unusual dividend or the repayment of share capital or a subordinated loan | |

| 4. Significant breaches of rules or other requirements under the Act, e.g. professional indemnity insurance cover being refused or cancelled. | |

- 01/12/2004

Core information where advance notice is required

MIGI 11.2.4

See Notes

| Notification | Supervision sourcebook (SUP) reference |

| A change in your firm's name | SUP 15.5.1 R |

| A change in address (to the principal place of business) | SUP 15.5.4 R |

| A

change to the legal status of your firm (You may be required to send us a new application for Part IV permission.) | SUP 15.5.5 R |

| A change to supervision by an overseas regulator | SUP 15.5.7 R |

- 01/12/2004

General notification requirements

MIGI 11.2.5

See Notes

| Breaches of rules and other requirements in or under the Act | SUP 15.3.11 R |

| Civil, criminal or disciplinary proceedings against a firm | SUP 15.3.15 R |

| Fraud, errors and other irregularities | SUP 15.3.17 R |

| Insolvency, bankruptcy and winding up | SUP 15.3.21 R |

| Change of accounting reference date | SUP 16.3.17 R |

| Change of controller | SUP 11.3 |

| Approved

persons: employees who start performing controlled functions, those who change

or add controlled functions or those who cease performing controlled functions. (There are standard forms to use called 'Approved Persons regime forms' - see Part I, paragraph 6.4.4.) | SUP 10.11 |

| Change of auditor (appointed under FSA rules) | SUP 3.3 |

- 01/12/2004

When should you notify us?

MIGI 11.2.6

See Notes

- 01/12/2004

How do you notify us?

MIGI 11.2.7

See Notes

- 01/12/2004

MIGI 11.2.8

See Notes

- 01/12/2004

MIGI 11.2.9

See Notes

- 01/12/2004

Other considerations

MIGI 11.2.10

See Notes

- 01/12/2004

MIGI 11.2.11

See Notes

| Authorisation - Part I, Chapter 4 |

| Complaints Reporting to the FSA - Part I, Chapter 14.3 |

- 01/12/2004