COLLG 5

The COLL sourcebook

COLLG 5.1

Introduction

- 01/12/2004

COLLG 5.1.1

See Notes

- 01/12/2004

The Collective Investment Schemes Sourcebook information guide

COLLG 5.1.2

See Notes

- 01/12/2004

Outline of the content of COLL

COLLG 5.1.3

See Notes

- 01/01/2006

Related Sourcebooks

COLLG 5.1.4

See Notes

- 01/12/2004

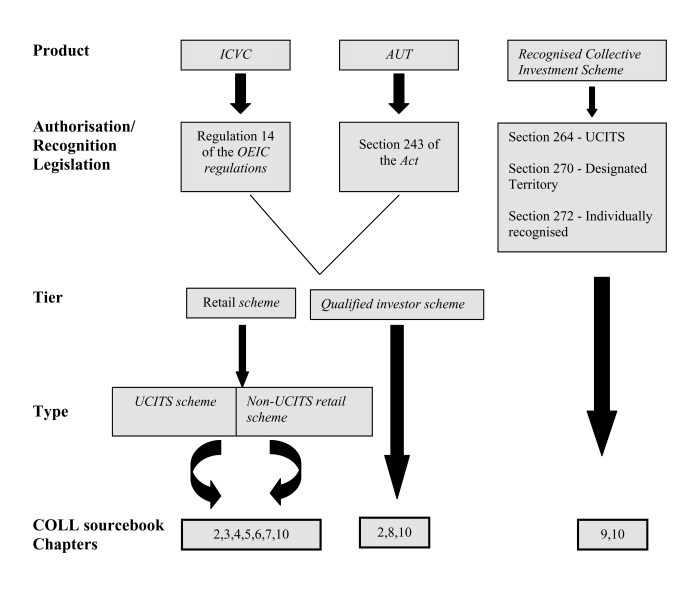

Function of the sourcebook: the two-tier regime

COLLG 5.1.5

See Notes

- 01/12/2004

Retail schemes

COLLG 5.1.6

See Notes

Retail schemes must be either UCITS schemes or non-UCITS retail schemes and COLL provides material relating to:

- (1) matters relating to authorisation and notification (COLL 2);

- (2) the constitution (COLL 3), investment powers (COLLG 5) and general management (COLL 6) of schemes and the arrangements for investor notification and participation (COLL 4);

- (3) how an authorised fund or sub-fund may suspend dealing in units or be wound up (COLL 7); and

- (4) fees payable in respect of them (FEES 1, FEES 2, FEES 3 and FEES 4).

- 01/01/2006

Qualified investor schemes

COLLG 5.1.7

See Notes

- 01/12/2004

Recognised schemes

COLLG 5.1.8

See Notes

- 01/01/2006