COLLG 1

Overview

COLLG 1.1

Introduction

- 01/12/2004

About this guide

COLLG 1.1.1

See Notes

- 01/12/2004

Structure of collective investment regulation in the UK

COLLG 1.1.2

See Notes

- 01/12/2004

What are regulated collective investment schemes?

COLLG 1.1.3

See Notes

- 01/12/2004

What are ICVCs?

COLLG 1.1.4

See Notes

- 01/12/2004

What are AUTs?

COLLG 1.1.5

See Notes

- 01/12/2004

Duties and responsibilities of the authorised fund manager and depositary

COLLG 1.1.6

See Notes

- 01/12/2004

Content of COLL 6.6 (Powers and duties of the scheme, the authorised fund manager, and the depositary)

COLLG 1.1.7

See Notes

- 01/12/2004

COLLG 2

European Legislation

COLLG 2.1

Introduction

- 01/12/2004

Background and scope

COLLG 2.1.1

See Notes

- 01/12/2004

General scope of the UCITS Directive

COLLG 2.1.2

See Notes

- 01/12/2004

Obligations on the management company and depositary

COLLG 2.1.3

See Notes

- 01/12/2004

COLLG 2.1.4

See Notes

- 01/12/2004

Investment and borrowing power limits

COLLG 2.1.5

See Notes

- 01/12/2004

Information to investors

COLLG 2.1.6

See Notes

- 01/12/2004

The management passport

COLLG 2.1.7

See Notes

- 01/12/2004

Marketing requirements (for UK firms)

COLLG 2.1.8

See Notes

- 01/12/2004

COLLG 3

The FSA's responsibilities under the Act

COLLG 3.1

Introduction

- 01/12/2004

COLLG 3.1.1

See Notes

- 01/12/2004

Marketing of schemes in the UK (section 238)

COLLG 3.1.2

See Notes

- 01/12/2004

Application for authorisation (section 242 and 243)

COLLG 3.1.3

See Notes

- 01/12/2004

COLLG 3.1.4

See Notes

- 01/12/2004

Notification of changes to unit trusts (section 251)

COLLG 3.1.5

See Notes

- 01/12/2004

Powers of intervention (section 257 and section281)

COLLG 3.1.6

See Notes

- 01/12/2004

Scheme particulars (section 248)

COLLG 3.1.7

See Notes

- 01/12/2004

Recognition of overseas schemes (section 264, 270 and 272)

COLLG 3.1.8

See Notes

- 01/12/2004

Subsequent notification in respect of schemes recognised under sections 270 and 272 of the Act

COLLG 3.1.9

See Notes

- 01/12/2004

Refusal of approval: schemes recognised under section270 and 272 of the Act

COLLG 3.1.10

See Notes

- 01/12/2004

Revocation of recognition of overseas schemes (section 279)

COLLG 3.1.11

See Notes

- 01/12/2004

Scheme facilities in the UK(section 283)

COLLG 4

The FSA's Responsibilities under the OEIC Regulations

COLLG 4.1

Introduction

- 01/12/2004

COLLG 4.1.1

See Notes

- 01/12/2004

Applications for authorisation (Regulations 12 - 17)

COLLG 4.1.2

See Notes

- 01/12/2004

Notification of changes to ICVCs (Regulation 21)

COLLG 4.1.3

See Notes

- 01/12/2004

Revocation of authorisation (Regulation 23)

COLLG 4.1.4

See Notes

- 01/12/2004

Power of intervention (Regulation 25)

COLLG 4.1.5

See Notes

- 01/12/2004

Corporate Code

COLLG 4.1.6

See Notes

- 01/12/2004

The FSA's Registration Function

COLLG 4.1.7

See Notes

- 01/12/2004

COLLG 5

The COLL sourcebook

COLLG 5.1

Introduction

- 01/12/2004

COLLG 5.1.1

See Notes

- 01/12/2004

The Collective Investment Schemes Sourcebook information guide

COLLG 5.1.2

See Notes

- 01/12/2004

Outline of the content of COLL

COLLG 5.1.3

See Notes

- 01/12/2004

Related Sourcebooks

COLLG 5.1.4

See Notes

- 01/12/2004

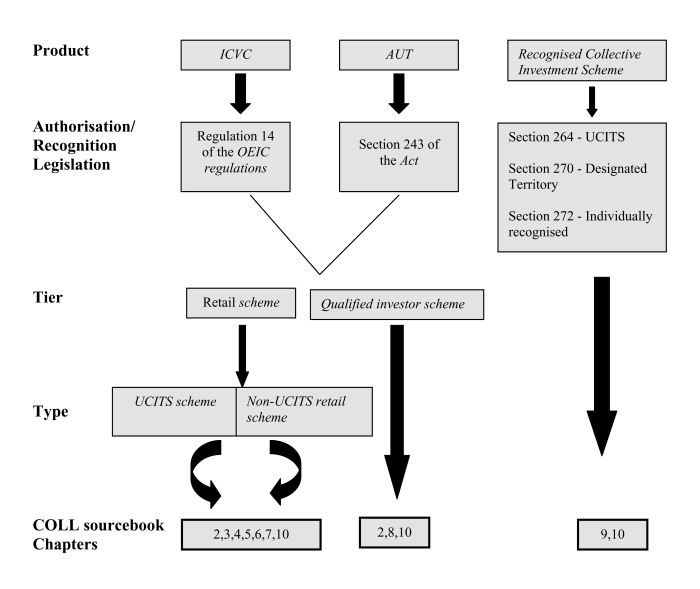

Function of the sourcebook: the two-tier regime

COLLG 5.1.5

See Notes

- 01/12/2004

Retail schemes

COLLG 5.1.6

See Notes

Retail schemes must be either UCITS schemes or non-UCITS retail schemes and COLL provides material relating to:

- (1) matters relating to authorisation and notification (COLL 2);

- (2) the constitution (COLL 3), investment powers (COLLG 5) and general management (COLL 6) of schemes and the arrangements for investor notification and participation (COLL 4);

- (3) how an authorised fund or sub-fund may suspend dealing in units or be wound up (COLL 7); and

- (4) fees payable in respect of them (COLL 10).

- 01/12/2004

Qualified investor schemes

COLLG 5.1.7

See Notes

- 01/12/2004

Recognised schemes

COLLG 5.1.8

See Notes

- 01/12/2004