COB 6

Product

disclosure and the customer's right to cancel or withdraw

COB 6.1

Product disclosure

- 01/12/2004

Application

COB 6.1.1

See Notes

COB 6.1 to COB 6.5 apply to a firm:

- (1) which sells, personally recommends or arranges (brings about) for the sale of a packaged product (other than units in a simplified prospectus scheme) to a private customer or to the trustees of an occupational pension scheme or to the trustee or operator of a stakeholder pension scheme; or

- (1A) which is an operator of a simplified prospectus scheme or which sells, personally recommends or arranges (brings about) for the sale of units in such a scheme to a client, whether or not held within a PEP or an ISA; or

- (2) which manages, sells or personally recommends a cash deposit ISA or cash deposit CTF for or to a private customer; or

- (3) which effects, personally recommends or arranges for a variation of a life policy for or to a private customer; or

- (4) which effects, personally recommends or arranges income withdrawals or short-term annuities for a private customer; or

- (5) which is a long-term insurer and receives:

- (a) a request from a private customer for a quotation for the surrender value of a life policy; or

- (b) any other indication that a private customer wishes to surrender a life policy: or

- (6) which receives a request from a private customer for a retirement quotation in respect of any of the following contracts provided by it:

- (a) a personal pension scheme;

- (b) a stakeholder pension scheme;

- (c) a free-standing additional voluntary contribution contract;

- (d) (where an open-market option is available under the contract terms) a retirement annuity contract; or

- (e) (where an open-market option is available under the contract terms) a pension buy-out contract; or

- (7) which enters into a distance contract with a retail customer to accept deposits.

- 06/04/2006

COB 6.1.1A

See Notes

- 09/10/2004

COB 6.1.2

See Notes

- (1) COB 6.2.21 R (Exceptions from the requirement to provide key features for life policies) and COB 6.2.24 R (Exceptions from the requirement to provide key features for key features schemes) contain exemptions from the requirement to produce key features in relation to life policies and key features schemes For simplified prospectus schemes COB 6.2.35 R (Exceptions from the requirement to provide the simplified prospectus) and COB 6.2.36 R (Exception from the requirement to provide a simplified prospectus: firms offering a funds supermarket service) contain similar exemptions from the requirement to provide a simplified prospectus.

- (2) COB 6.4.3 G to COB 6.4.5 G and COB 6.4.19 R to COB 6.4.20 G set out how the rules apply where packaged products are sold to the trustees of certain occupational pension schemes or to the trustees or operators of stakeholder pension schemes.

- 01/10/2005

Application of COB 6.2.46R and COB 6.2.47R

COB 6.1.2A

See Notes

- 01/05/2005

Purpose

COB 6.1.3

See Notes

- 09/10/2004

Requirement to produce key features

COB 6.1.4

See Notes

- (1) A product provider or stakeholder pension scheme operator must, for each packaged product which it offers produce key features which, as to design and content, comply with the requirements of COB 6.1, COB 6.2 and COB 6.5.

- (2) A firm to which COB 6.4.13 (1) applies must, for each cash deposit ISA or cash deposit CTF it offers, produce the information document required by COB 6.5.42 R or COB 6.5.42A instead of key features. That information document must comply with COB 6.1, COB 6.2 and COB 6.5 as to design and content.

- (3) (1) does not apply in relation to a simplified prospectus scheme.

- 09/10/2004

Quality and production of key features

COB 6.1.5

See Notes

A firm must ensure that any key features or information document it produces in relation to a packaged product, cash deposit ISA or cash deposit CTF is in writing, whether in printed hard copy or in electronic format, and:

- (1) is produced and presented to at least the same quality and standard as the associated sales or marketing material being used by the firm to promote the packaged product, cash deposit ISA or cash deposit CTF to customers; and

- (2) is separate from any other material given to the customer, unless it is produced for a key features scheme , stakeholder pension scheme, or personal pension scheme other than a personal pension policy; in that case it may be included as part of another item of sales or marketing material, but only if the key features or information document appears with due prominence.

- 06/04/2007

COB 6.1.6

See Notes

- 01/12/2001

COB 6.2

Provisions of key features or simplified prospectus

- 01/05/2005

Application

COB 6.2.1

See Notes

- 01/12/2001

Medium for provision of key features

COB 6.2.2

See Notes

- 09/10/2004

COB 6.2.3

See Notes

- 01/12/2001

COB 6.2.4

See Notes

- 01/05/2005

COB 6.2.5

See Notes

- 01/12/2001

COB 6.2.5A

See Notes

- 01/05/2005

Life policies

COB 6.2.6

See Notes

- 01/12/2001

COB 6.2.7

See Notes

- 01/10/2005

COB 6.2.8

See Notes

- 01/12/2001

Exception for life policies: sales through intermediaries

COB 6.2.9

See Notes

COB 6.2.7 R does not apply to a product provider when its life policy is sold on the personal recommendation of, or arranged to be sold by, another person, provided that other person:

- (1) is a firm (or appointed representative) operating from an establishment maintained by the firm (or appointed representative) in the United Kingdom; or

- (2) is operating from an establishment in an EEA State whose law imposes an obligation on the person to provide information about the life policy in accordance with articles 3 and 5(1) and (2) of the Distance Marketing Directive.

- 09/10/2004

Life policies: pre-completion variations

COB 6.2.12

See Notes

- (1) Where key features have already been provided by a firm to a private customer in accordance with COB 6.2.7 and the terms for the proposed life policy are subsequently altered before the private customer completes an application form, the firm must ensure that the private customer is provided with revised key features, unless the alteration is one or more of the following:

- (a) the amount of the premium is changed;

- (b) the amount of any commission or remuneration payable is reduced;

- (c) a rider benefit is added, removed or amended.

- (2) If (1)(a) to (c) apply, then, subject to COB 6.4.27 to COB 6.4.31 (telephone sales and other exemptions), if the contract is to be a distance contract with a retail customer, the retail customer must be provided with details of such changes in a durable medium in good time before the contract is concluded.

- 09/10/2004

COB 6.2.13

See Notes

- 01/12/2001

COB 6.2.14

See Notes

- 09/10/2004

COB 6.2.15

See Notes

- 09/10/2004

Variations to existing life policies

COB 6.2.16

See Notes

When a policyholder applies to vary a life policy issued on or after 1 January 1995 (or is recommended to do so) and the variation of the policy gives rise to a right to cancel under COB 6.7.7 R, the policy holder must be provided with:

- (1) the information required by COB 6.5.15 R to COB 6.5.19 R, COB 6.5.23 R to COB 6.5.25 R, COB 6.5.27 R to COB 6.5.28 R and COB 6.5.38 R; and

- (2) in the case of a variation which results in a new distance contract, all the contractual terms and conditions and the information in COB App 1;

in a durable medium by the firm personally recommending, arranging or effecting the variation in good time before it is put into effect, unless COB 6.2.19 R (sales through intermediaries) or COB 6.4.27 R to COB 6.4.31 R (telephone sales and other exemptions) applies.

- 09/10/2004

COB 6.2.16A

See Notes

- (1) When a long-term care insurance contract which is

- (a) not a pure protection contract and which was issued on or after 1 January 1995; or

- (b) a pure protection contract and which was issued on or after 31 October 2004;

- is varied so as to bring into effect provisions for long-term care benefits, the firm must provide the private customer with appropriate key features in good time sufficient to enable the private customer to consider them before the variation takes effect.

- (2) If the circumstances of the variation, whether by the exercise of an option or otherwise, make it impossible to provide the key features before the variation takes effect, the firm must do so as soon as possible afterwards.

- 31/10/2004

COB 6.2.17

See Notes

- 09/10/2004

COB 6.2.18

See Notes

- (1) When a policyholder applies to vary:

- (a) a life policy issued before 1 January 1995; or

- (b) a pure protection contract issued before 31 October 2004 and which would after 30 October 2004 be a long-term care insurance contract;

- (or is personally recommended to do so) and the variation of the policy gives rise to a right to cancel under COB 6.7.7 R, information must be given to the policyholder by the firm that is personally recommending, arranging or effecting the variation before it is put into effect, unless COB 6.2.19 R or COB 6.4.27 R to COB 6.4.31 R (telephone sales and other exemptions) applies.

- (2) When giving the information in (1), the firm must:

- (a) believe on reasonable grounds that the information given is sufficient to enable the policyholder to understand the consequences of the variation; and

- (b) in the case of a variation which results in a new distance contract, in good time before the variation is put into effect, provide all the contractual terms and conditions and the information in COB App 1.

- 31/10/2004

COB 6.2.19

See Notes

COB 6.2.16 R and COB 6.2.18 R do not apply to a product provider when the variation to its life policy is effected on the personal recommendation of or arranged by another person, provided that other person:

- (1) is a firm (or appointed representative) operating from an establishment maintained by the firm (or appointed representative) in the United Kingdom; or

- (2) is operating from an establishment in an EEA State whose law imposes an obligation on the person to provide information about the variation to the life policy in accordance with articles 3 and 5(1) and (2) of the Distance Marketing Directive.

- 09/10/2004

Exception for life policies: non-UK customers

COB 6.2.21

See Notes

There is no requirement for key features to be provided for a new life policy or a variation to an existing policy if, at the time that the private customer signs the application, he is habitually resident:

- (1) (except for distance contracts with retail customers) in an EEA State other than the United Kingdom; or

- (2) outside the EEA and he is not present in the United Kingdom.

- 09/10/2004

Exceptions for life policies: variations held within a CTF

COB 6.2.21A

See Notes

COB 6.2.7 does not apply to a CTF provider in relation to a variation to an existing policy held within a CTF, if:

- (1) the terms and conditions, including all charges, are the same as applied at the time of the purchase, or the most recent purchase or payment, of the existing policy; and

- (2) key features outlining those terms and conditions were issued to the customer in respect of that previous purchase.

- 01/12/2001

Provision of key features: key features schemes

COB 6.2.22

See Notes

- (1) When a firm sells, personally recommends or arranges for the sale of a key features scheme to a private customer, unless COB 6.2.24 R (exceptions) or COB 6.4.27 R to COB 6.4.31A R (telephone sales and other exemptions) applies, the private customer must be provided with appropriate key features for the scheme before he completes an application for the scheme holding.

- (2) (1) does not apply where the operator of the scheme has elected that the scheme will comply with COB 6.2.26 R to COB 6.2.45A R instead of the provisions in COB 6 that relate to key features.

- (3) (2) does not apply to an investment trust.

- 01/10/2005

COB 6.2.23

See Notes

- (1) COB 6.2.22 R applies not just to new purchases but also to any recommendation or application to transfer the value of a particular fund holding within a key features scheme to a different fund within the same scheme.

- (2) Where a private customer has responded to a direct offer financial promotion, the mailing package or direct offer financial promotion should have included example-based key features - there is no requirement to provide a further set of key features to such a private customer in respect of the same transaction.

- 01/10/2005

Exceptions from the requirement to provide key features for key features schemes

COB 6.2.24

See Notes

A firm need not provide key features to a private customer in respect of a key features scheme if:

- (1) the firm is a product provider and the scheme holding is sold on the personal recommendation of, or arranged to be sold by another person, provided that other person:

- (a) is a firm (or appointed representative) operating from an establishment maintained by the firm (or appointed representative) in the United Kingdom; or

- (b) is operating from an establishment in an EEA State whose law imposes obligations on the person to provide information about the scheme holding in accordance with articles 3 and 5(1) and (2) of the Distance Marketing Directive; or

- (2) at the time he signs the application, the private customer is habitually resident outside the EEA and is not present in the United Kingdom; or

- (3) (except for distance contracts with retail customers) the scheme holding is purchased by a private customer on an execution-only basis; or

- (4) the scheme holding is purchased on behalf of a private customer by an investment manager exercising discretion; or

- (5) the sale of the scheme holding is arranged or recommended by an investment manager who is not exercising discretion and the private customer has agreed, either in relation to that specific holding or generally, that key features need not be provided; or

- (6) a private customer is making a purchase of a scheme holding (whether or not held within a CTF) in a key features scheme in which he already has a scheme holding and has already been provided with appropriate key features covering the purchase; or

- (7) a private customer is transferring from accumulation units to income units of the same scheme (or vice versa) and has already been supplied with key features which cover the transfer.

- 01/10/2005

Purpose of the COB 6 provisions on the simplified prospectus

COB 6.2.25A

See Notes

- 01/05/2005

Production and publication of simplified prospectus

COB 6.2.26

See Notes

- (1) An operator of a simplified prospectus scheme must, for each simplified prospectus scheme in respect of which it is the operator, produce and publish a simplified prospectus in accordance with the rules in this section and ensure that it contains in summary form each of the matters referred to in COB 6.2.37 R.

- (2) A simplified prospectus must be incorporated in a written document or in any durable medium.

- (3) An operator of a simplified prospectus scheme must be satisfied on reasonable grounds that each simplified prospectus which it produces:

- (a) includes all such information as is necessary to enable an investor to make an informed decision about whether to acquire units in the scheme;

- (b) does not omit any key item of information;

- (c) wherever possible is written in plain language which avoids technical language and jargon; and

- (d) adopts a format and style of presentation which is clear and attractive to the average reader, so that it can be easily understood by him.

- (4) The simplified prospectus may be attached to the full prospectus as a removable part of it.

- (5) [deleted]

- (6) [deleted]

- 01/10/2005

Revision of simplified prospectus

COB 6.2.27

See Notes

- 01/05/2005

COB 6.2.28

See Notes

- 01/05/2005

Filing requirements

COB 6.2.29

See Notes

A UCITS management company must for each UCITS scheme it manages file the scheme's initial simplified prospectus, together with each revision to it, with:

- (1) the FSA; and

- (2) the competent authority of each EEA state in which its units are to be marketed in the exercise of an EEA right.

- 01/05/2005

UK firms exercising passporting rights in respect of UCITS scheme

COB 6.2.30

See Notes

- (1) A UCITS management company must for each UCITS scheme it manages and in respect of which it is marketing units in another EEA State in the exercise of an EEA right, produce a simplified prospectus for the scheme drawn up in accordance with the requirements contained in this section.

- (2) The simplified prospectus must be drawn up in the, or one of the, official languages of the EEA State for which it was prepared or in a language approved by the competent authority of that State.

- (3) The simplified prospectus may, without alteration, be used for marketing purposes in the EEA State for which it was prepared and in which the units of the simplified prospectus scheme are to be sold.

- 01/05/2005

COB 6.2.31

See Notes

- (1) In translating the simplified prospectus from English into the or one or more of the official languages of the EEA State in which the simplified prospectus scheme is to be marketed, or into a language approved by the competent authority of that State, it is permissible under article 28.3 of the UCITS Directive, as amended, in the FSA's view, for figures expressed in pounds sterling to be converted into the appropriate local currency such as euros. It is not necessary, for example, for the simplified prospectus of a scheme that is to be marketed across the EEA in the exercise of an EEA right, to have to refer to each amount in pounds sterling, in euros and additionally in every other local currency of an EEA State in which units of the scheme are to be marketed that has not adopted the euro as its currency.

- (2) Operators considering marketing the units of their simplified prospectus schemes in another EEA State in the exercise of an EEA right should have regard to the local marketing legislation of such country.

- 01/10/2005

Offering a simplified prospectus

COB 6.2.32

See Notes

- (1) When a firm sells, personally recommends or arranges (brings about) for the sale of a simplified prospectus scheme, it must offer the scheme's up-to-date simplified prospectus free of charge to any person who may become a subscriber to the scheme before a contract for the sale of units is concluded.

- (2) The requirement in (1) will be met by a firm in relation to a private customer if it or any other firm provides him with a copy of the simplified prospectus in accordance with COB 6.2.33 R (1).

- 01/05/2005

Obligation on a firm to provide a simplified prospectus

COB 6.2.33

See Notes

- (1) When a firm sells, personally recommends or arranges (brings about) for the sale of a simplified prospectus scheme to a private customer in the United Kingdom, the firm must provide him with the up-to-date simplified prospectus for the scheme before he completes an application for the scheme holding unless COB 6.2.35 R or COB 6.2.36 R or COB 6.4.27 R to COB 6.4.31A R (telephone sales and other exemptions) apply.

- (2) (1) does not apply to a UCITS management company when it sells units in a UCITS scheme without personally recommending or arranging for the sale of such units.

- 01/10/2005

COB 6.2.34

See Notes

- (1) COB 6.2.33 R applies not just to new purchases but also to any recommendation or application to transfer the value of a particular fund holding within a scheme to a different sub-fund within the same scheme.

- (2) Where a private customer has responded to a direct offer financial promotion, the mailing package or direct offer financial promotion should have included the simplified prospectus for the scheme, in which case there is no requirement to provide a further simplified prospectus to such a private customer in respect of the same transaction.

- (3) COB 6.2.33 R may apply to either the operator or the distributor of a simplified prospectus scheme depending on how units in the scheme are to be sold.

- (4) Where one of the exceptions in COB 6.2.35 R or COB 6.2.36 R applies, firms should bear in mind that they must still comply with COB 6.2.32 R (Offering a simplified prospectus) which represents an absolute requirement of the UCITS Directive and as such, cannot be made subject to any exclusions. For example, a firm offering a funds supermarket service which is entitled to the benefit of the exception in COB 6.2.36 R must ensure that every private customer is offered the simplified prospectus of each relevant simplified prospectus scheme before a contract for the sale of units is concluded.

- 01/05/2005

Exceptions from the requirement to provide the simplified prospectus

COB 6.2.35

See Notes

A firm need not, unless a private customer specifically requests it, provide a simplified prospectus to a private customer for a simplified prospectus scheme if:

- (1) the firm is a product provider and the scheme holding is sold on the personal recommendation of, or arranged to be sold on the personal recommendation of, or arranged to be sold by another person, provided that other person:

- (a) is a firm (or appointed representative) operating from an establishment maintained by the firm (or appointed representative) in the United Kingdom; or

- (b) is operating from an establishment in an EEA State whose law imposes obligations on the person to provide information about the scheme holding in accordance with articles 3 and 5(1) and (2) of the Distance Marketing Directive; or

- (2) at the time the private customer signs the application, the private customer is habitually resident outside the EEA and is not present in the United Kingdom; or

- (3) (except for distance contracts with retail customers) the scheme holding is purchased by the private customer in the course of an execution-only transaction; or

- (4) the scheme holding is purchased on behalf of the private customer by an investment manager exercising discretion; or

- (5) the sale of the scheme holding is arranged or recommended by an investment manager who is not exercising discretion and the private customer has agreed, either in relation to that specific holding or generally, that the simplified prospectus need not be provided; or

- (6) a private customer is making a purchase of a scheme holding (whether or not held within a CTF) in a scheme in which he already has a scheme holding and has already been provided with the up-to-date simplified prospectus which covers the purchase; or

- (7) a private customer is transferring from accumulation units to income units of the same scheme (or vice versa) and has already been supplied with the up-to-date simplified prospectus of the scheme which covers the transfer.

- 01/05/2005

Exception from the requirement to provide a simplified prospectus: firms offering and intermediaries selling a funds supermarket service

COB 6.2.36

See Notes

- (1) A firm to which COB 6.2.33 R (Obligation on a firm to provide a simplified prospectus) applies when it:

- (a) offers a funds supermarket service; or

- (b) sells, personally recommends or arranges (brings about) the sale of a simplified prospectus scheme through a funds supermarket service;

- need not, unless a private customer requests it, provide a private customer with a simplified prospectus for any simplified prospectus scheme to which the funds supermarket service relates provided it complies with the condition in (2).

- (2) The condition is that the firm must instead provide the private customer with the abbreviated form of composite key features document that is permitted under COB 6.5 (Content of key features) and which covers each of the key features schemes and simplified prospectus schemes to which the funds supermarket service relates.

- 01/10/2005

COB 6.2.37

See Notes

Contents of the simplified prospectus

This table belongs to COB 6.2.26 R (1)

| Contents of simplified prospectus | ||||

| Note: | This table sets out the required contents of the simplified prospectus. It reproduces Schedule C (Contents of the simplified prospectus) of the Management Company Directive (2001/107/EC), as amplified by the Commission Recommendation (2004/384/EC). This Table also includes, and cross-refers to, other material which the FSA considers should be included. |

|||

| Brief presentation of the simplified prospectus scheme (in this Table referred to as "the scheme"). | ||||

| (1) | when the scheme was created and an indication of the EEA State where the scheme has been registered or incorporated; | |||

| (2) | in the case of a scheme having different investment compartments (sub-funds), the indication of this circumstance; | |||

| (3) | the name and contact details of the operator (when applicable); | |||

| (4) | the expected period of existence of the scheme (when applicable); | |||

| (5) | the name and contact details of the depositary; | |||

| (6) | the name and contact details of the auditors; | |||

| (7) | the name and brief details of the financial group (e.g. a bank) promoting the scheme; | |||

| Investment information | ||||

| (8) | a short description of the scheme's objectives including: | |||

| (a) | a concise and appropriate description of the outcomes sought for any investment in the scheme; | |||

| (b) | a clear statement of any guarantees offered by third parties to protect investors and any restrictions on those guarantees; and | |||

| (c) | a statement, where relevant, that the scheme is intended to track an index or indices, and sufficient information to enable investors both to identify the relevant index or indices and to understand the extent or degree of tracking pursued; | |||

| Notes: | 1. | Information on (8)(a) should include a statement as to whether there is any arrangement intended to result in a particular capital or income return from the units or any investment objective of giving protection to their capital value or income return and, if so, details of that arrangement or protection. | ||

| 2. | The information disclosed under (8)(b) should include an explanation of what is to happen when an investment is encashed before the expiry of any related guarantee or protection. | |||

| (9) | the scheme's investment policy, including: | |||

| (a) | the main categories of eligible financial instruments which are the object of investment; | |||

| (b) | whether the scheme has a particular strategy in relation to any industrial, geographic or other market sectors or specific classes of assets, e.g. investments in emerging countries' financial instruments; | |||

| (c) | where relevant, a warning that, whilst the actual portfolio composition is required to comply with the broad legal and statutory rules and limits, risk-concentration may occur in regard of certain tighter asset classes, economic and geographic sectors; | |||

| (d) | if the scheme invests in bonds, an indication of whether they are corporate or government, their duration and the ratings requirements; | |||

| (e) | if the scheme uses financial derivative instruments, an indication of whether this is done in pursuit of the scheme's objectives, or for hedging purposes only; | |||

| (f) | whether the scheme's management style makes some reference to a benchmark; and in particular whether the scheme has an 'index tracking' objective, with an indication of the strategy to be pursued to achieve this; and | |||

| (g) | whether the scheme's management style is based on a tactical asset allocation with high frequency portfolio adjustments; | |||

| provided the information is material and relevant; | ||||

| Note: | The information referred to in paragraphs (8) and (9) may be set out as a single item in the simplified prospectus (e.g. for the information on index tracking), provided that the information so combined does not lead to confusion of the objectives and policies of the scheme. The order of the information items may be adapted to reflect the scheme's specific investment objectives and policy. | |||

| (10) | a brief assessment of the scheme's risk profile by investment compartment or sub-fund, including: | |||

| (a) | overall structure of the information provided: | |||

| (i) | a statement to the effect that the value of investments may fall as well as rise and that investors may get back less than they put in; | |||

| (ii) | a statement that details of all the risks actually mentioned in the simplified prospectus may be found in the full prospectus; | |||

| (iii) | a description in words of any risk investors have to face in relation to their investment, but only where such risk is relevant and material, based on risk impact and probability; and | |||

| (b) | details regarding the description (in words) of the following risks: | |||

| (i) | specific risks: | |||

| The description referred to in paragraph (10)(a)(iii) should include a brief and understandable explanation of any specific risk arising from particular investment policies or strategies or associated with specific markets or assets relevant to the scheme such as: | ||||

| A | the risk that the entire market of an asset class will decline thus affecting the prices and values of the assets (market risk); | |||

| B | the risk that an issuer or a counterparty will default (credit risk); | |||

| C | only where strictly relevant, the risk that a settlement in a transfer system does not take place as expected because a counterparty does not pay or deliver on time or as expected (settlement risk); | |||

| D | the risk that a position cannot be liquidated in a timely manner at a reasonable price (liquidity risk); | |||

| E | the risk that the investment's value will be affected by changes in exchange rates (exchange or currency risk); | |||

| F | only where strictly relevant, the risk of loss of assets held in custody that could result from the insolvency, negligence or fraudulent action of the custodian or of a subcustodian (custody risk); and | |||

| G | risks related to a concentration of assets or markets; and | |||

| (ii) | horizontal risk factors: | |||

| The description referred to in paragraph (10)(a)(iii) should also mention, where relevant and material, the following factors that may affect the product: | ||||

| A | performance risk, including the variability of risk levels depending on individual fund selections, and the existence, absence of, or restrictions on any guarantees given by third parties; | |||

| B | risks to capital, including potential risk of erosion resulting from withdrawals/cancellations of units and distributions in excess of investment returns; | |||

| C | exposure to the performance of the provider/third-party guarantor, where investment in the product involves direct investment in the provider, rather than assets held by the provider; | |||

| D | inflexibility, both within the product (including early surrender risk) and constraints on switching to other providers; | |||

| E | inflation risk; and | |||

| F | lack of certainty that environmental factors, such as a tax regime, will persist; | |||

| (iii) | possible prioritisation of information disclosure: | |||

| In order to avoid conveying a misleading image of the relevant risks, the information items should be presented so as to prioritise, based on scale and materiality, the risks so as to better highlight the individual risk profile of the scheme; | ||||

| (11) | the historical performance of the scheme (where applicable) and a warning that this is not an indicator of future performance (which may be either included in or attached to the simplified prospectus), including: | |||

| (a) | disclosure of past performance: | |||

| (i) | the scheme's past performance, as presented using a bar chart showing annual returns for the last ten full consecutive years. If the scheme has been in existence for fewer than ten years but at least for a period of one year, it is recommended that the annual returns, calculated net of tax and charges, be given for as many years as are available; and | |||

| (ii) | if a scheme is managed according to a benchmark or if its cost structure includes a performance fee depending on a benchmark, the information on the past performance of the scheme should include a comparison with the past performance of the benchmark according to which the scheme is managed or the performance fee is calculated; | |||

| Note: | Comparison should be achieved by representing the past performance of the benchmark and that of the scheme through the use of appropriate graphs to assist the reader to make the comparison. | |||

| (b) | disclosure of cumulative performance: | |||

| Disclosure should be made of the cumulative performance of the scheme over the ten year period referred to in paragraph (11)(a)(i). A comparison should also be made with the cumulative performance (where relevant) of a benchmark, when comparison to a benchmark is required in accordance with paragraph (11)(a)(ii); | ||||

| Note: | Where the scheme has been in existence for fewer than ten years but at least for a period of one year, disclosure of the past cumulative performance should be made for as many years as are available. | |||

| (c) | exclusion of subscription and redemption fees, subject to appropriate disclosure: | |||

| A statement should be made that past performance of the scheme does not include the effect of subscription and redemption fees. | ||||

| Notes: | 1. | Where a comparison is being made with the cumulative performance of a benchmark as required by paragraph (11)(b), the comparison should be achieved by representing the past performance of the benchmark and that of the scheme through the use of appropriate graphs to assist the reader to make the comparison. | ||

| 2. | The scheme's historical performance may be produced as a separate attachment to the simplified prospectus. | |||

| (12) | a profile of the typical investor the scheme is designed for; | |||

| Economic information | ||||

| (13) | the scheme's applicable tax regime, including: | |||

| (a) | the tax regime applicable to the scheme in the UK; and | |||

| (b) | a statement which explains that the regime of taxation of the income or capital gains received by individual investors depends on the tax law applicable to the personal situation of each individual investor and/or to the place where the capital is invested and that if investors are unclear as to their fiscal position, they should seek professional advice or information from local organisations, where available; | |||

| Note: | This information should include a statement in relation to SDRT provision, explaining how the scheme may suffer stamp duty reserve tax as a result of transactions in units and whether the operator's policy is such that an SDRT provision may be imposed. | |||

| (14) | details of any entry and exit commissions relating to the scheme and details of the scheme's other possible expenses or fees, distinguishing between those to be paid by the unitholder and those to be paid from the scheme's or the sub-fund's assets, including: | |||

| (a) | overall contents of the information provided: | |||

| (i) | disclosure of a total expense ratio (TER), calculated as indicated in COB 6 Annex 2 R, except for a newly created fund where a TER cannot yet be calculated; | |||

| (ii) | on an ex ante basis, disclosure of the expected cost structure, that is an indication of all costs available according to the list set forth in COB 6 Annex 2 R so as to provide investors, in so far as possible, with a reasonable estimate of expected costs; | |||

| (iii) | all entry and exit commissions and other expenses directly paid by the investor; | |||

| (iv) | an indication of all the other costs not included in the TER, including disclosure of transaction costs; | |||

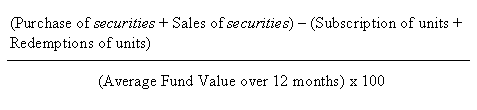

| (v) | as an additional indicator of the importance of transaction costs, the portfolio turnover rate, calculated as shown in COB 6 Annex 3 R; and | |||

| (vi) | an indication of the existence of fee-sharing agreements and soft commissions; | |||

| Notes: | 1. | In explaining the function of the TER to the reader, appropriate wording should be used in the simplified prospectus. For example, TER might be explained in the following terms: "The TER shows the annual operating expenses of the scheme - it does not include transaction expenses. All European funds highlight the TER to help you compare the annual operating expenses of different schemes." |

||

| 2. | It is the FSA's understanding that the disclosure of a reasonable estimate of expected costs on an ex ante basis, as required by paragraph (14)(a)(ii), only applies to new schemes where a TER cannot yet be calculated. Where a TER can be calculated for a simplified prospectus scheme, there is no need to have to disclose a reasonable estimate of expected costs on an ex ante basis in accordance with paragraph (14)(a)(ii), in addition to the TER. | |||

| 3. | In disclosing details of all entry and exit commissions relating to the fund and details of the scheme's other possible expenses or fees, the firm must present the information in the format required by COB 6.2.38 R (1) (Reduction in yield). Compliance with this rule will ensure that the information is presented in the form of an impact of charges table based on reduction in yield figures, so as to assist the comprehension of the reader. | |||

| 4. | Paragraph (14)(a)(vi)) should not be interpreted as a general validation of the compliance of any individual agreement or commission with the provisions of the Handbook . Taking into account current market practice, consideration should be given as to how far the scheme's existing fee-sharing agreements and comparable fee arrangements are for the exclusive benefit of the scheme. | |||

| 5. | The simplified prospectus should make a reference to the full prospectus for detailed information on these kinds of arrangements, which should allow any investor to understand to whom expenses are to be paid and how possible conflicts of interest will be resolved in his/her best interest. The information provided in the simplified prospectus should remain concise in this respect. | |||

| (b) | information about 'fee sharing agreements' and 'soft commissions': | |||

| (i) | identification of 'fee-sharing agreements'; | |||

| Note: | For the purposes of paragraph (14)(b)(i), fee-sharing agreements should be taken as those agreements whereby a party remunerated, either directly or indirectly, out of the assets of a scheme agrees to split its remuneration with another party and which result in that other party meeting expenses through this fee-sharing agreement that should normally be met, either directly or indirectly, out of the assets of the scheme. | |||

| (ii) | identification of soft commissions; | |||

| Note: | For the purposes of paragraph (14) (b) (ii), soft commissions should be regarded as any economic benefit, other than clearing and execution services, that an asset manager receives in connection with the scheme's payment of commissions on transactions that involve the scheme's portfolio securities. Soft commissions are typically obtained from, or through, the executing broker. | |||

| (c) | presentation of TER and portfolio turnover rate; | |||

| Note: | Both the TER and the portfolio turnover rate may be either included in or attached to the simplified prospectus in the same paper as information on past performance. | |||

| Commercial information | ||||

| (15) | how to buy the units; | |||

| Note: | This should include an explanation of any relevant right to cancel or withdraw from the purchase, or, where it is the case, that such rights do not apply. | |||

| (16) | how to sell the units; | |||

| (17) | in the case of a scheme having different investment compartments (sub-funds), an explanation of how to switch from one investment compartment into another and any charges applicable in such cases; | |||

| (18) | when and how dividends on units or shares of the scheme (if applicable) are distributed; | |||

| (19) | when and where prices of units are published or made available; | |||

| Additional information | ||||

| (20) | a statement that, on request, the full prospectus and the annual and half-yearly reports of the scheme may be obtained free of charge before the conclusion of the contract and afterwards, together with details of how they may be obtained or how a person may gain access to them; | |||

| (21) | the name and contact details of the FSA as being the competent authority which has authorised or registered the scheme; | |||

| (22) | details of a contact point (person or department, and, if appropriate the times of day etc.) where additional information may be obtained if needed; | |||

| (23) | the date of publication of the simplified prospectus. | |||

| General Note: | ||||

| In making the disclosures required by paragraphs (8) to (19) of this Table, the information must be presented in the form of questions and answers. This format is designed to assist the comprehension of the reader. This requirement will not apply in relation to a simplified prospectus that is to be used to market the units of the scheme in another EEA state or in relation to a simplified prospectus that is to be used to market the units of the scheme exclusively to persons who are not private customers. | ||||

- 01/10/2005

Reduction in yield

COB 6.2.38

See Notes

- (1) In disclosing the information required by paragraph (14) of COB 6.2.37 R (Table: Contents of the simplified prospectus), a firm should set out the information in the format required by, and include the contents of, COB 6.5.30 R (Table for key features schemes) to COB 6.5.35 R (Calculation method for "effect of charges to date" for key features schemes) and COB 6.5.38 R (Commission and commission equivalent for life policies, key features schemes and stakeholder pension schemes), as if such provisions applied to simplified prospectus schemes, as modified by COB 6.2.39 R (Table).

- (2) Where the units of a simplified prospectus scheme are to be marketed and sold in another EEA State, or exclusively to persons who are not private customers, the operator of the scheme need not comply with the requirements in (1) for the simplified prospectus that is to be used to market the scheme in that EEA State.

- (3) Note 3 to paragraph (14) of COB 6.2.37 R (Table: Contents of the simplified prospectus) and COB 6.2.38 R to COB 6.2.40 G cease to have effect on 30 June 2009, unless re-made.

- 01/10/2005

COB 6.2.39

See Notes

Application of COB 6.5.30R to COB 6.5.35R, and COB 6.5.38R

This table belongs to COB 6.2.38R

| Application of COB 6.5.30 R to COB 6.5.35 R, and COB 6.5.38 R | ||

| Rule | Description | Modification |

| COB 6.5.31 R | Table | Substitute "COB 6.2.43 R (1)" for the reference to COB 6.5.15 R (2). |

| COB 6.5.32 R (1), (2) and (3) | Scheme projections | Substitute "COB 6.2.43 R (1)" for the references to COB 6.5.15 R (2). |

| COB 6.5.32 R (3) and COB 6.5.32 R (7)(a) | Scheme projections | Substitute "client" for the references to "private customer". |

- 01/05/2005

COB 6.2.40

See Notes

- 01/05/2005

Distance contracts for the sale of simplified prospectus schemes

COB 6.2.41

See Notes

- 01/05/2005

COB 6.2.42

See Notes

- 01/10/2005

Projection for simplified prospectus scheme

COB 6.2.43

See Notes

- (1) When a firm sells, personally recommends or arranges for the sale of a simplified prospectus scheme to a private customer and the proposed transaction is for a scheme:

- (a) which relates to an election to make income withdrawals or purchase of a short-term annuity; or

- (b) where the private customer's primary objective is to acquire:

- (i) a specified sum of money on a specified date; or

- (ii) a specified sum of money on death; or

- (iii) an annuity of a specified amount payable as from a specified date;

- the firm must provide the private customer with a projection, illustrating how the principal terms of the proposed transaction apply to him.

- (2) (1) does not apply to a UCITS management company when it sells units in a UCITS scheme without personally recommending or arranging for the sale of such units.

- (3) (1) does not apply to a direct offer financial promotion in relation to units in a simplified prospectus scheme.

- 06/04/2006

COB 6.2.44

See Notes

- 01/05/2005

PEP and ISA investments

COB 6.2.45

See Notes

- (1) When a firm sells, personally recommends or arranges for the sale of a unit in a simplified prospectus scheme to a private customer which is to be held within a PEP or ISA, it must provide him with the following additional information:

- (a) a description of the nature of the services the firm will provide for the private customer in relation to the PEP or ISA;

- (b) [deleted]

- (c) [deleted]

- (d) a statement that the favourable tax treatment of ISAs may not be maintained;

- (e) how and when statements (if any) will be sent;

- (f) an explanation how the ISA or plan may be terminated or transferred to another ISA or PEP manager;

- (g) whether the ISA is a mini or maxi-ISA agreement and an explanation of the differences between the two; and

- (h) whether the private customer has a choice to reinvest income, where uninvested money will be held and whether interest is paid on such money.

- (2) (1) does not apply to a UCITS management company when it sells units in a UCITS scheme without personally recommending or arranging for the sale of such units.

- (3) (1) does not apply to the extent that a private customer is making a purchase of a scheme holding in a simplified prospectus scheme in which he already has a scheme holding and has already been provided with the information set out at (1)(a) to (h) which remains up-to-date.

- 01/05/2005

Child trust fund investments

COB 6.2.45A

See Notes

- 01/10/2005

UCITS Directive: requirement to offer a simplified prospectus for section 264 schemes

COB 6.2.46

See Notes

- (1) When a firm sells, personally recommends or arranges (brings about) for the sale of a UCITS scheme which is a recognised scheme under section 264 of the Act (Schemes constituted in other EEA States) to a client, it must offer the client free of charge a copy of the scheme's most recent simplified prospectus before an application for the scheme holding is completed.

- (2) The simplified prospectus must meet the requirements of the UCITS Directive necessary for the scheme to enjoy the rights conferred by the Directive.

- (3) When the scheme holding is purchased on behalf of a client by an investment manager exercising discretion, the requirement in (1) will be satisfied by the investment manager being offered the simplified prospectus free of charge before the application form for a scheme holding is completed.

- (4) A firm must not carry on any of the activities referred to in (1) in relation to a UCITS scheme which is a recognised scheme under section 264 of the Act unless it is satisfied on reasonable grounds that:

- (a) the scheme's simplified prospectus has been sent to the FSA before any units in the scheme are marketed in the UK; and

- (b) the information contained in the simplified prospectus is up-to-date and is not in need of revision;

- and that any subsequent amendments thereto have been sent to the FSA.

- 01/10/2005

Sale of a section 264 scheme by distance contract

COB 6.2.47

See Notes

- 01/05/2005

Composite documents for several schemes, sub-funds and classes

COB 6.2.48

See Notes

- 01/10/2005

Multiclass schemes: use of representative class

COB 6.2.49

See Notes

- 01/10/2005

COB 6.3

Post-sale confirmation: life policies

- 01/12/2004

Application

COB 6.3.1

See Notes

- 20/09/2001

COB 6.3.2

See Notes

- 01/12/2001

COB 6.3.3

See Notes

- 01/12/2001

COB 6.3.4

See Notes

- 01/12/2001

COB 6.3.5

See Notes

- 09/10/2004

Exceptions to post-sale confirmation

COB 6.3.6

See Notes

A long-term insurer need not send or give the post-sale confirmation required by COB 6.3.3 R when:

- (1) the long-term insurer has taken reasonable steps to determine that the life policy or variation is purchased or effected on behalf of a private customer by an investment manager exercising discretion; or

- (2) the life policy is purchased by the trustees of an occupational pension scheme; or

- (3) the life policy is purchased by the trustees or manager of a stakeholder pension scheme or if the life policy is otherwise sold as a stakeholder product;

- (4) a life policy issued before 1 January 1995 is being varied; or

- (5) at the time the private customer signs the application for the new life policy or variation, he is habitually resident:

- (a) in an EEA State other than the United Kingdom; or

- (b) outside the EEA and he is not present in the United Kingdom.

- 06/04/2005

COB 6.4

Product disclosure: special situations

- 01/12/2004

Application

COB 6.4.1

See Notes

- 06/04/2007

COB 6.4.2

See Notes

- 01/05/2005

Occupational pension schemes

COB 6.4.3

See Notes

- 01/05/2005

COB 6.4.4

See Notes

- (1) When a firm sells, personally recommends or arranges the sale of a new group or master life policy, the first in a series of individual life policies or the first units in a particular key features scheme or simplified prospectus scheme to or for the trustees of a money-purchase occupational scheme, it must provide the trustees with key features, in accordance with COB 6.2.7 R to COB 6.2.25 R or for a simplified prospectus scheme, with a simplified prospectus, in accordance with COB 6.2.26 R to COB 6.2.45 R.

- (2) In COB 6.2 to COB 6.5, for the purposes of (1), the firm must treat the trustees as private customers.

- (3) In addition to the information to be provided to trustees under COB 6.4.4 R (1), the firm must ensure that key features or the simplified prospectus are made available to the trustees to distribute to all scheme members at the outset of the scheme and for subsequent new members.

- (4) The requirement in COB 6.4.4 R (3) applies to main scheme benefits and to additional voluntary contributions where members' benefits are linked to earmarked segments of life policies or schemes. It does not apply where trustees make pooled investments and make their own arrangements for allocation of investment returns to determine members' benefits, whether attached to defined benefit pension schemes or money purchase occupational scheme.

- 01/10/2005

COB 6.4.5

See Notes

- (1) The illustrative figures within the key features provided under COB 6.4.4 R (1) can be on an example basis, using a range of representative actual or hypothetical scheme members (covering, for example, different ages, sexes and salaries), so that the trustees can assess the effectiveness of the investment for their pension scheme members.

- (2) The definition of money-purchase occupational scheme includes executive pension plans (established for directors, executives and senior employees), small self-administered schemes that provide money-purchase benefits and additional voluntary contribution schemes.

- (3) Group personal pension schemes are not occupational pension schemes and COB 6.4.4 R does not apply to them. Firms should therefore provide each person who is offered membership of a group personal pension scheme with key features or a simplified prospectus in accordance with COB 6.1 and COB 6.2. This does not preclude generic key features being sent out as part of a financial promotion, provided that a post-sale confirmation is issued in accordance with COB 6.3.3 R.

- (4) The objective of COB 6.4.4 R (3) is to ensure that prospective scheme members have access to information about the occupational pension scheme that could enable comparison with alternative personal investments. Firms may decide for themselves the format (but not content) of this information. For example, individual sets of key features can be supplied or a schedule of details which the trustees or their advisers can assimilate into other pension scheme communications.

- 01/05/2005

SIPPs, personal pension deposits and personal pension products

COB 6.4.5A

See Notes

When a firm sells, manages, personally recommends or arranges the sale of a SIPP, personal pension deposit or personal pension product (not the assets within them) to or for a private customer, the firm must, unless COB 6.4.27 R to COB 6.4.31A R apply, provide the private customer with:

- (1) sufficient information about the relevant scheme for the private customer to be able to make an informed decision before that customer completes an application for that scheme; and

- (2) (in respect of a distance contract with a retail customer) the relevant contractual terms and conditions and the information set out in COB App 1,

in a durable medium in good time before the customer is bound by the transaction.

- 06/04/2007

COB 6.4.5B

See Notes

- 06/04/2007

COB 6.4.5C

See Notes

COB 6.4.5A R does not apply to a scheme operator when its scheme is sold on the personal recommendation of, or arranged to be sold by, another person, provided that other person:

- (1) is a firm (or an appointed representative) operating from an establishment maintained by the firm (or appointed representative) in the United Kingdom; or

- (2) is operating from an establishment in an EEA State whose law imposes an obligation on the person to provide information about the scheme in accordance with articles 3 and 5(1) and (2) of the Distance Marketing Directive.

- 06/04/2007

Assets to be held within a SIPP

COB 6.4.5D

See Notes

Where a firm makes a personal recommendation to a private customer about the purchase of an asset to be held within a SIPP, the firm must, unless COB 6.4.27 R to COB 6.4.31A R applies, provide the private customer with:

- (1) sufficient information about that asset, and the risks and advantages of the proposed asset purchase, for the customer to be able to make an informed decision about the asset purchase before it takes place; and

- (2) in respect of a distance contract with a retail customer) the relevant contractual terms and conditions and the information set out in COB App 1;

in a durable medium in good time before the customer is bound by the transaction.

- 06/04/2007

COB 6.4.5E

See Notes

- 06/04/2007

Sales of life policies (etc.) to operators of personal pension schemes

COB 6.4.6

See Notes

- (1) A firm which sells, personally recommends or arranges the sale of a new group or master life policy, the first in a series of individual life policies or the first units in a particular key features scheme or simplified prospectus scheme to the operator of a personal pension scheme, must provide the operator of that scheme with key features (in accordance with COB 6.2.7 R to COB 6.2.25 R) or a simplified prospectus (in accordance with COB 6.2.26 R to COB 6.2.45 R), as the case may be.

- (2) In COB 6.2 to COB 6.5, for the purposes of (1), members, prospective members and trustees must be treated by the firm as private customers.

- 06/04/2007

COB 6.4.6A

See Notes

- 06/04/2007

Income withdrawals and short-term annuities

COB 6.4.8

See Notes

- 06/04/2007

COB 6.4.8A

See Notes

When a firm personally recommends, arranges or effects an income withdrawal from a SIPP, personal pension deposit or personal pension product to or for a private customer, it must provide that customer with:

- (1) sufficient information about the income withdrawal for the customer to be able to make an informed decision; and

- (2) (in respect of a distance contract with a retail customer), the relevant contractual terms and conditions and the information set out in COB App 1,

in a durable medium in good time before the customer is bound by the transaction.

- 06/04/2007

COB 6.4.8B

See Notes

- 06/04/2007

COB 6.4.9

See Notes

In relation to an election to make income withdrawals, or short-term annuities, the requirement for the provision of key features or a simplified prospectus in:

- (1) COB 6.2.7 R also applies when an existing life policy is to be endorsed;

- (2) COB 6.2.22 R or, for simplified prospectus schemes, COB 6.2.33 R also applies when an existing scheme holding is to be used.

- 06/04/2006

COB 6.4.10

See Notes

- 06/04/2006

COB 6.4.11

See Notes

- 06/04/2007

COB 6.4.12

See Notes

Where income is being taken, no less than six weeks before the end of the annuity period for a short-term annuity or at intervals no longer than 12 months from the date of an election by a private customer to make income withdrawals the product provider of the unvested pension scheme must:

- (1) provide the private customer with such information required by COB 6.6.13 R as will enable the private customer to review the options available; and

- (2) inform the private customer how to obtain advice on investments in respect of his unsecured or alternatively secured pension, and that it would be in his best interests to do so.

- 06/04/2006

Cash deposit ISAs and cash deposit CTFs

COB 6.4.13

See Notes

- 09/10/2004

Traded life policies

COB 6.4.14

See Notes

- 09/10/2004

Stakeholder pension schemes

COB 6.4.15

See Notes

- 01/10/2005

COB 6.4.16

See Notes

- 01/12/2001

COB 6.4.17

See Notes

- 01/12/2001

COB 6.4.18

See Notes

COB 6.4.15 R does not apply to a stakeholder pension scheme operator when its stakeholder pension scheme is sold on the personal recommendation of, or arranged to be sold by, another person, provided that other person:

- (1) is a firm (or an appointed representative) operating from an establishment maintained by the firm (or appointed representative) in the United Kingdom; or

- (2) is operating from an establishment in an EEA State whose law imposes an obligation on the person to provide information about the stakeholder pension scheme in accordance with articles 3 and 5(1) and (2) of the Distance Marketing Directive.

- 09/10/2004

COB 6.4.19

See Notes

- (1) When a firm sells, personally recommends or arranges the sale of a new group or master life policy, the first in a series of individual life policies or the first units in a particular key features scheme or simplified prospectus scheme to the trustees or the operator of a stakeholder pension scheme, it must provide the trustees or operator with key features, in accordance with COB 6.2.7 R to COB 6.2.25 R or for a simplified prospectus scheme, with a simplified prospectus, in accordance with COB 6.2.26 R to COB 6.2.45 R.

- (2) In COB 6.2 to COB 6.5, for the purposes of (1), the firm must treat trustees and operators as private customers.

- 01/10/2005

COB 6.4.20

See Notes

- 01/12/2001

COB 6.4.21

See Notes

- 01/12/2001

COB 6.4.22

See Notes

- 09/10/2004

COB 6.4.23

See Notes

The notice in COB 6.4.22 R must:

- (1) confirm that no advice on investment has been given and that the private customer has decided that the stakeholder pension scheme is appropriate as a result of the answers he has given to the questions posed in the decision tree; and

- (2) include a copy of the decision tree indicating the answers which the private customer has given.

- 01/12/2001

COB 6.4.24

See Notes

- 01/12/2001

Entering into a distance contract for accepting deposits (other than a cash deposit ISA or a personal pension deposit)

COB 6.4.25

See Notes

- 06/04/2007

Exemption: telephone sales

COB 6.4.27

See Notes

- (1) Where this chapter requires key features, a simplified prospectus or other information to be provided, in the case of voice telephony communications, a firm:

- (a) must provide the customer at the beginning of the telephone conversation with the name of the firm and (if the call is initiated by the firm) the commercial purpose of the call;

- (b) provided the customer gives his explicit consent to receiving only limited information, may proceed on the basis of at least the following information:

- (i) the name of the person in contact with the customer and his link with the firm;

- (ii) a description of the main characteristics of the service;

- (iii) the total price to be paid by the customer to the firm for the service, including all related fees, charges and expenses, and all taxes paid through the firm together with a statement, where relevant, that commission or remuneration will be paid to the adviser or representative, or, where an exact price cannot be indicated, the basis for the calculation of the price enabling the customer to verify it;

- (iv) where relevant, notice of the possibility that other taxes or costs may exist that are not paid through the firm or imposed by it;

- (v) the existence or absence of a right to cancel the service under COB 6.7 and, where there is such a right, its duration and the conditions for exercising it, including information on the amount which the customer may be required to pay if the contract is terminated early or unilaterally under its terms, as well as the consequences of not exercising it; and

- (vi) that other information is available on request, and the nature of that information, and

- (vii) in addition to (a) and (b) above, where the product is a CTF, provided the customer gives his explicit consent to receiving only limited information, may proceed on the basis of the information referred to in COB 6.5.40 R (7) given orally.

- (2) If the customer does not give his explicit consent to receiving limited information, and the parties wish to proceed by telephone, the firm must prior to the conclusion of the contract provide all of the information required by COB App 1 orally to the customer.

- (3) In the case of either (1) or (2), the firm must send the private customer immediately after the contract is concluded, the required key features, simplified prospectus or other information (as applicable) in a durable medium.

- 01/05/2005

COB 6.4.28

See Notes

- 09/10/2004

Exemption: certain other means of distance communication

COB 6.4.29

See Notes

- 01/05/2005

Exemption: successive or separate operations under an initial service agreement

COB 6.4.30

See Notes

- 01/05/2005

Exemption: other successive and separate operations

COB 6.4.31

See Notes

This exemption applies where this chapter requires a key features, simplified prospectus or other information to be provided in relation to a distance contract, if:

- (1) the firm has no initial service agreement with the customer:

- (2) the firm has performed an operation for the customer within the last year: and

- (3) the contract is in relation to a successive operation or separate operation of the same nature (see COB 1.10.2 G (2)).

- 01/05/2005

Exemption: automatic enrolment of employees in pension schemes

COB 6.4.31A

See Notes

- 06/04/2007

COB 6.4.32

See Notes

At each anniversary of the date on which a long-term care insurance contract which is based on single premium investment bonds was entered into, the insurer must:

- (1) provide the private customer with a table based on the format of COB 6.5.24 containing at least the current fund value and projected future policy values (as in column "What you might get back");

- (2) where it is the case, inform the private customer of the possibility that future policy values may be insufficient to fulfil the original purpose of the contract; and

- (3) inform the private customer how to obtain advice on investments in respect of long-term care insurance contracts, and that it is in his best interest to do so.

- 01/12/2001

COB 6.4.33

See Notes

In the case of a long-term care insurance contract in which:

- (1) long-term care benefits are available after commencement of the policy at the option of the policyholder; and

- (2) as a result of the exercise of that option a new contract of insurance is offered to the policyholder;

provision is made in TC 2.5.5A R so that, in respect of the contract containing the option, an employee, although engaged in advising on long-term care insurance contracts need not be required to pass an appropriate examination for long-term care insurance contracts to do so.

- 01/12/2001

Exemption: Revenue allocated accounts

COB 6.4.34

See Notes

- 01/12/2001

COB 6.4.35

See Notes

- 01/12/2001

COB 6.5

Content of key features and important information: life policies, key features schemes, ISA and CTF cash deposit components and stakeholder pension schemes

- 01/10/2005

Application

COB 6.5.1

See Notes

- 01/12/2001

General

COB 6.5.2

See Notes

A firm must ensure, unless COB 6.5.3 R applies, that:

- (1) the key features it produces for a life policy or a key features scheme other than a stakeholder pension scheme (whether or not held within a PEP or an ISA) includes the information required by COB 6.5.11 R, set out in the order shown divided by appropriate and prominent sub-headings, some of which are prescribed in the rules;

- (2) the information it produces under COB 6.4.13R (1) for a cash deposit ISA or cash deposit CTF complies with whichever of COB 6.5.42 R or COB 6.5.42A applies to it;

- (3) the information document or abbreviated form of key features it produces:

- (a) relating to friendly society tax exempt policies or traded life policies contains the applicable information specified in COB 6.5.43 R- COB 6.5.44;

- (b) relating to broker funds contains the applicable information in COB 6.5.45;

- (4) the post-sale confirmation document it produces contains the applicable information specified in COB 6.5.46 R;

- (5) the key features it produces or issues for a stakeholder pension scheme:

- (a) includes the relevant sub-headings set out at COB 6.5.11 R, the applicable information specified in COB 6.5.12 R - COB 6.5.40 R appropriate to those sub-headings; and

- (b) is, subject to COB 6.5.6 R, accompanied by or includes the decision trees specified in COB 6.5.8 R, unless the stakeholder pension scheme is being purchased as a result of a personal recommendation; and

- (6) all:

- (a) key features; and

- (b) abbreviated key features mentioned at COB 6.5.2 (3)(a) above,

- it produces in relation to a distance contract with a retail customer include or are accompanied by all the contractual terms and conditions and the information in COB App 1 except to the extent that they are separately provided to the retail customer in a durable medium in good time before the retail customer is bound by the contract or offer.

- 01/10/2005

COB 6.5.3

See Notes

- 09/10/2004

COB 6.5.4

See Notes

- (1) Where the rules in COB 6.5 do not require the use of prescribed text, firms may give the relevant information using their own words and style.

- (2) For the purposes of COB 6.5.2 R (1):

- (a) a firm which offers more than one key features scheme may choose whether to produce separate key features for each scheme (including a fund or sub-fund or share class), or to produce a single key features to cover a range of funds (provided the differences between those funds are made clear);

- (b) where a publication covers more than one key features scheme (for example, in the case of a year book comprising information on all the funds offered by a unit trust manager), it might consist of a key features section at the beginning giving details common to all the relevant funds (whether unit trusts, ICVCs, sub-funds of an umbrella scheme or share classes within an ICVC), followed by separate pages setting out, for each fund, those items which are specific to it, for example 'Aims', 'Risk Factors' and 'Charges and their Effect'.

- 01/10/2005

Stakeholder pension schemes: decision trees

COB 6.5.5

See Notes

- 01/08/2002

COB 6.5.6

See Notes

- 01/12/2001

COB 6.5.7

See Notes

- 01/12/2001

COB 6.5.8

See Notes

- (1) Whether a firm produces decision trees within or separate from key features, it must (unless COB 6.5.9 R applies and subject to COB 6.5.8A R) reproduce the text, content and format set out in COB 6 Annex 1.

- (2) If COB 6 Annex 1 is subsequently amended:

- (a) the firm must amend its decision trees as soon as reasonably practicable and, in any case, within three months of the date when the amendments to COB 6 Annex 1 come into force; and

- (b) the firm may continue to use decision trees that complied with the previous version of COB 6 Annex 1 until it has done so.

- 01/08/2002

COB 6.5.8A

See Notes

A firm must ensure that its decision trees include:

- (1) (in the place in the relevant table in the Further information text at COB 6 Annex 1 where the square brackets appear):

- (a) in the heading of the table, the current tax year; and

- (b) the Basic State Pension rates and Pension Credit minimum income rates for the current tax year;

- (2) (where the square brackets appear) at the bottom of the cover page and at the bottom of each page of the flow charts, the current tax year; and

- (3) (where the square brackets appear) in the introductory text where additional explanatory text within Further information is signposted, the appropriate page number.

- 01/05/2004

COB 6.5.8B

See Notes

- (1) A firm must, subject to (2), make the changes required by COB 6.5.8A R as soon as reasonably practicable and, in any case, within three months of the start of the tax year.

- (2) Where, in any year, a firm is required to make changes to the trees under COB 6.5.8 R and COB 6.5.8A R, it may make both sets of changes at the same time, provided that it does so within the time limits in COB 6.5.8 R (2)(a).

- 01/08/2002

COB 6.5.8C

See Notes

- (1) The FSA expects to review the decision trees once each year and will amend them as necessary as near as possible to the start of the new tax year. The amended version of the decision trees will be published on the FSA's web-site and available in printed form when the rules are amended each year. Firms must bring their trees into line with the amended rules within three months, but may continue to use their "old" trees until they have done so.

- (2) Firms are required, by COB 6.5.8A R, to insert the Basic State Pension rates and Minimum Income Guarantee rates for the current tax year into the relevant table in the introductory text to their decision trees each year and to identify the relevant year in the heading of the table and also at the bottom of the pages specified in COB 6.5.8A R (2). The rules require firms to do this within three months of the start of the tax year if no other changes to the trees are required. However, COB 6.5.8B R (2) allows them to delay updating the Basic State Pension and Minimum Income Guarantee rates until the same time as they make any other amendments to their trees which they are required to make under COB 6.5.8 R, provided that they do so within no more than three months of the date when those amendments come into force.

- (3) The appropriate rates will be those announced by the Government (usually, but not necessarily, in the Chancellor of the Exchequer's annual Budget) as applying to the tax year in question. The relevant Basic State Pension and Minimum Income Guarantee rates for the current tax year will be included in the version of the trees published by the FSA.

- 01/08/2002

COB 6.5.8D

See Notes

- 01/08/2002

COB 6.5.8E

See Notes

- 01/08/2002

COB 6.5.8F

See Notes

- 01/08/2002

COB 6.5.9

See Notes

- 01/08/2002

COB 6.5.10

See Notes

- (1) There is a limited scope within COB 6.5.9 R to depart from the prescribed decision tree format and content in order to blend in the trees with other promotional materials such as key features or internet financial promotions. However, the text and general design should follow the prescribed content and format. Firms will be aware that the FSA publishes its own version of the decision trees for public use: firms may consider them as examples of acceptable design.

- (2) Examples of items and formatting where no adaptations should be made include:

- (a) the text - both content and order, whether in the introduction, the boxes within the flowcharts, or any other sections of the decision trees;

- (b) the use of boxed items within the introductory text;

- (c) the use of emphasis (firms can choose the method of giving emphasis, such as size, bold or italic text);

- (d) the vertical flow and pagination of the flowcharts within the decision trees;

- (e) the boxes within the flowchart pages, these should be rectangular and filled with one consistent colour, except that two tints of the base colour may be used to highlight tick boxes and to differentiate columns of figures;

- (f) the directional arrows linking the boxes within flowchart pages, these should be of one design and the same colour as fills the flowchart boxes.

- (3) Examples of items where adaptations can be made include:

- (a) the typeface and font size of the text;

- (b) the pagination of the introductory text and the use of columns;

- (c) the edging of boxes (for example, use of shadow or rounded corners);

- (d) the use of background colours, for example, to match corporate colours or product brochures (see (2)(e));

- (e) separate colour schemes to differentiate between sets of decision trees, for example between employed and self-employed versions;

- (f) the use of an extra colour to highlight headings within flowchart pages and to identify separate versions of the decision trees;

- (g) the size of paper used (A4 is recommended, but other sizes are possible, provided that the flowchart pages are clear and legible);

- (h) where delivery is through an interactive computer-based system, the wording of the introductory text that explains how to use the decision trees.

- 01/12/2001

COB 6.5.11

See Notes

Table of Information/Applicable provisions

This table belongs to COB 6.5.2 R (1)

| Information | Applicable provisions | ||

| Title | COB 6.5.12 R | ||

| Nature of life policy or key features scheme or stakeholder pension scheme | COB 6.5.13 R - COB 6.5.14 G | ||

| An example | COB 6.5.15 R - COB 6.5.19 R | ||

| Description of the life policy or key features scheme or stakeholder pension scheme | COB 6.5.20 R | ||

| Tables: | Life policies Key features schemes |

COB 6.5.23 R - COB 6.5.26 R COB 6.5.30 R - COB 6.5.32 R |

|

| Deductions summary: | Life policies Key features schemes |

COB 6.5.27 R - COB 6.5.29 R COB 6.5.33 R - COB 6.5.36 G |

|

| Commission and remuneration | COB 6.5.38 R - COB 6.5.39 G | ||

| Further information | COB 6.5.40 R | ||

- 01/10/2005

Title

COB 6.5.12

See Notes

- 01/10/2005

Nature of life policy or key features scheme or stakeholder pension scheme

COB 6.5.13

See Notes

- (1) A firm must describe the nature of the life policy or key features scheme or stakeholder pension scheme under the following headings: 'its aims', 'your commitment', or, 'your investment' (whichever is more appropriate) and 'risk factors'.

- (2) Under 'risk factors' a firm must give a brief description of the factors which may have an adverse effect on performance or are otherwise material to the decision to invest.

- 01/10/2005

COB 6.5.14

See Notes

The description which a firm is required to provide under 6.5.13R(2) might include information on the matters set out in the following non-exhaustive list:

- (1) whether the value of the capital and any income from it might fluctuate;

- (2) cancellation issues, including the fact that, if the value of the investment falls before notice of cancellation is given, a full refund of the original investment may not be provided but rather the original amount less the fall in value;

- (3) particular risks, if any, associated with the underlying assets in which the packaged product is invested;