CIS App 1

Correction of box management errors

CIS App 1.1

Appendix

- 01/12/2004

CIS App 1.1.1

See Notes

Correction of box management errors

| 1 | Introduction | ||

| Application | |||

| (1) | This appendix applies to authorised fund managers and to depositaries. | ||

| (2) | This appendix is the appendix referred to in CIS 4.3.8 G (Box management errors) and CIS 15.3.3 G (Box management errors). | ||

| 2 | Controls by authorised fund managers and depositaries | ||

| Controls by authorised fund managers | |||

| (1) | An authorised fund manager needs to be able to demonstrate that it has effective controls over: | ||

| (a) | its calculations of what units are owned by it (its "box"); and | ||

| (b) | compliance with the rules preventing a negative box (CIS 4.3.9 R (2), CIS 4.3.10 R (2), CIS 15.3.4 R (3), CIS 15.3.7 R (3), CIS 4.3.12 R and CIS 15.3.12 R). | ||

| (2) | Evidence of persistent or repetitive errors in relation to these matters, and in particular any evidence of a pattern of errors working in an authorised fund manager's favour, will make demonstrating effective controls more difficult. | ||

| Controls by depositaries | |||

| (3) | A depositary has a duty under CIS 7.4.1 R (General duties of the depositary) and CIS 7.9.1 R (Oversight by the trustee of the manager) to ensure (for an AUT) that the manager of an AUT is operating the AUT in accordance with the rules in this sourcebook, including CIS 4 or CIS 15, and to ensure (for an ICVC) that the ICVC is managed in accordance with CIS 4. | ||

| (4) | A depositary should therefore make a regular assessment of the authorised fund manager's box management procedures (including supporting systems) and controls. This should include reviewing the authorised fund manager's controls and procedures when the depositary assumes office, on any significant change and on a regular basis, to ensure that a series of minor changes do not have a significant effect on the accuracy of the controls and procedures. | ||

| 3 | Recording and reporting of box management errors | ||

| (1) | An authorised fund manager should record all errors which are made in the calculation of an authorised fund manager's box which result in a breach of: | ||

| (a) | CIS 4.3.9 R (2) (Issue of units to meet authorised fund manager's obligation to sell); | ||

| (b) | CIS 4.3.10 R (2) (Cancellation and payment for cancelled units); | ||

| (c) | CIS 15.3.4 R (3) (Issue of units: manager's instructions); and | ||

| (d) | application | ||

| and as soon as an error is discovered, the authorised fund manager should report the fact to the depositary, together with details of the action taken, or to be taken, to avoid repetition of the error. | |||

| (2) | The authorised fund manager should also report to the depositary immediately any box management errors that do not result in a breach, but would be material under (3). | ||

| (3) | A depositary should report material box management errors to the FSA immediately. Materiality should be determined by taking into account a number of factors including: | ||

| (a) | the existence of sufficient controls put into place by the authorised fund manager; | ||

| (b) | the significance of any breakdown in management controls or other checking procedures; | ||

| (c) | the significance of any failure of systems. This may include situations where inadequate back-up arrangements exist; | ||

| (d) | the duration of an error; and | ||

| (e) | the level of compensation due to holders, and an authorised fund manager's ability (or otherwise) to meet claims for compensation in full. | ||

| (4) | A depositary should also make a return to the FSA (in the manner prescribed by SUP 16.6.13R) on a quarterly basis summarising, by authorised fund manager amongst other things, the number of box management errors during a particular period where a depositary does not consider the breach to have been an isolated error, whether or not the error results in a negative box. | ||

| 4 | Correction of box management errors where no compensation is required | ||

| (1) | Correction of errors in calculating an authorised fund manager's box, may only be made, without an obligation to compensate holders, when: | ||

| (a) | the error is an isolated error, and is unlikely to recur; | ||

| (b) | the authorised fund manager can demonstrate that it has effective controls in place over box management, including all the areas which affect the figures which are included in the box management calculations; and | ||

| (c) | the requirements of CIS 4.3.12 R (Modification to number of units issued or cancelled) for single-priced AUTs and ICVCs, or CIS 15.3.12 R (Modification to number of units issued or cancelled) for dual-priced AUTs, are complied with. | ||

| (2) | In addition, no compensation is required if an error resulted in a larger positive box, because this would not have caused a breach of the rules. | ||

| 5 | Correction of box management errors where compensation to the authorised fund may be required | ||

| Paragraph 4(1) may not apply (for example, because there have been persistent errors, or an individual error has been discovered too late, or the depositary is not satisfied about the effectiveness of the authorised fund manager's systems). In these circumstances, not only should all errors be corrected as soon as possible, but compensation is required to the extent that (a) to (e): | |||

| (A) | error results from an under-issue | ||

| Where a negative box results from an under-issue of units - units sufficient to correct the negative box must immediately be issued, unless this requirement has already been satisfied by subsequent issues or by redemptions subsequent to the under-issue. If the price (or, for a dual-priced AUT, the issue price has risen, no compensation is required. If the price (or, for a dual-priced AUT, the issue price) has fallen, the authorised fund manager must compensate the authorised fund for the difference in price (or, for a dual-priced AUT, the issue price) between the valuation point at which the issue should have been made and the valuation point when the under-issued position was extinguished. | |||

| (B) | error results from an over-cancellation and the price or (for a dual-priced AUT the cancellation price) has risen | ||

| Where an error results from an over-cancellation, and the price (or, for a dual-priced AUT, the cancellation price) has risen, the error will be automatically corrected with no further penalty, since, when the error is discovered, an authorised fund manager must either undertake an issue of units, or cancel a lower number of units, or cover the error by redemptions, all at a higher price (or, for a dual-priced AUT, the cancellation price). | |||

| (C) | error results from an over-cancellation and the price or (for a dual-priced AUT cancellation price) has fallen | ||

| Where the price (or, for a dual-priced AUT, the cancellation price) has fallen, an authorised fund manager is required to rectify the breach immediately by arranging an issue of units, if it has not already been rectified by a subsequent issue, or covered by subsequent redemptions. An authorised fund manager should compensate the authorised fund for the difference between the price (or, for a dual-priced AUT, the cancellation price when the over-cancellation was made and the price (or, for a dual-priced AUT, the cancellation price) when it was rectified, irrespective of whether corrected by issue, lower subsequent cancellation, or redemptions. | |||

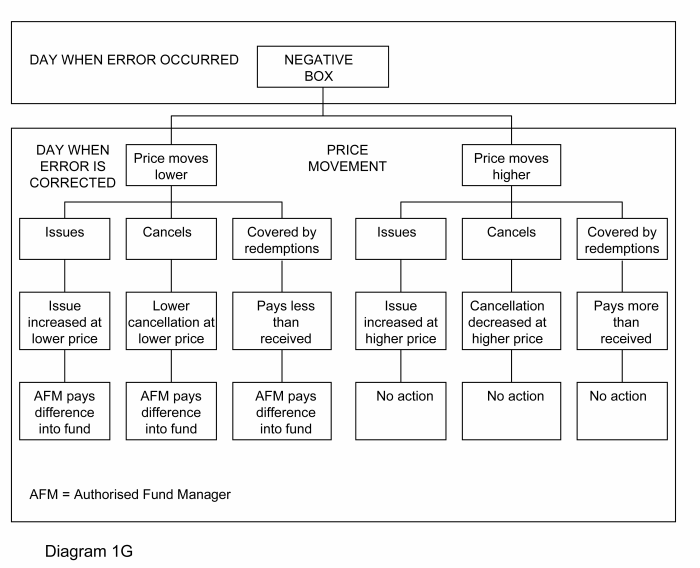

| (D) | diagram | ||

| Diagram 1G sets out the action required under (b) when the price (or, in the case of a dual-priced AUT, cancellation price) has moved higher and under (c) when the price (or, in the case of a dual-priced AUT, cancellation price) has moved lower. | |||

| (E) | de minimis provision for late issue settlement of AUTs | ||

| Where interest due on an isolated instance of a late issue settlement amounts to a figure which is lower than £25, this may be waived if, in the depositary's opinion, there will be no material effect on the authorised fund, and the depositary is satisfied with the authorised fund manager's system of controls. | |||

- 01/12/2004