CIS 15

Dual-pricing and dealing

CIS 15.1

Introduction

- 01/12/2004

Application

CIS 15.1.1

See Notes

- (1) This chapter applies in relation to dual-priced AUTs. Accordingly, in this chapter:

- (a) references to "AUTs" and to "units" relate only to dual-priced AUTs and to units in them; and

- (b) references to "manager" or "trustee" relate only to the manager or trustee of a dual-priced AUT.

- (2) This section (CIS 15.1) applies to managers and trustees.

- (3)

- (a) If, and to the extent that, the authorised fund manager and the depositary so agree, income units and accumulation units are to be treated, for the purposes in (b) as belonging to the same class of units.

- (b) The only purposes to which (a) can apply are:

- (i) ascertaining the number of units respectively to be issued or cancelled in order for the authorised fund manager to comply with CIS 15.3.4 R (3) (Issue of units to meet authorised fund managers obligation to sell) and CIS 15.3.7 R (3) (Cancellation and payment for cancelled units); and

- (ii) Compliance with requirements of this chapter relating to information to be given by the authorised fund manager to the depositary.

- (c) Paragraphs (a) and (b) do not apply to the income units and accumulation units of an AUT unless the rights attached to those classes provide for their prices to be calculated by reference to undivided shares (howsoever called) in a manner similar to that resulting from CIS 2.6.1 R (Units and classes of units in AUTS).

- 01/12/2004

CIS 15.1.2

See Notes

- 01/12/2004

Purpose

CIS 15.1.3

See Notes

- 01/08/2002

Explanation

CIS 15.1.4

See Notes

- 01/12/2004

CIS 15.2

Initial offers and unitisations

- 01/12/2004

Application

CIS 15.2.1

See Notes

- 01/12/2004

Purpose

CIS 15.2.2

See Notes

- 01/12/2004

Period of initial offer

CIS 15.2.3

See Notes

- 01/12/2004

Issue of units: initial offer

CIS 15.2.4

See Notes

- 01/12/2004

Initial price

CIS 15.2.5

See Notes

- 01/12/2004

Compulsory termination of initial offer

CIS 15.2.6

See Notes

- 01/12/2004

Creation of units: unitisation

CIS 15.2.7

See Notes

- 01/12/2004

CIS 15.3

Issues and cancellations

- 01/12/2004

Application

CIS 15.3.1

See Notes

- 01/12/2004

Purpose

CIS 15.3.2

See Notes

- 01/12/2004

Box management errors

CIS 15.3.3

See Notes

- 01/12/2004

Issue of units: manager's instructions

CIS 15.3.4

See Notes

- 01/11/2002

Issue by trustee

CIS 15.3.5

See Notes

- 01/12/2004

Issue price

CIS 15.3.6

See Notes

- 01/12/2004

Cancellation of units

CIS 15.3.7

See Notes

- 01/12/2004

Cancellation price

CIS 15.3.8

See Notes

- 01/12/2004

Trustee's refusal to issue or cancel units

CIS 15.3.9

See Notes

- 01/11/2002

Instructions or notifications between manager and trustee

CIS 15.3.10

See Notes

- 01/12/2004

Timing of instructions to issue or cancel units

CIS 15.3.11

See Notes

- 01/12/2004

Modification to number of units issued or cancelled

CIS 15.3.12

See Notes

- 01/12/2004

CIS 15.4

Sale and redemption

- 01/12/2004

Application

CIS 15.4.1

See Notes

- 01/12/2004

Purpose

CIS 15.4.2

See Notes

- 01/12/2004

Manager's obligation to sell

CIS 15.4.3

See Notes

- 01/04/2004

Sale price parameters

CIS 15.4.4

See Notes

- 01/12/2004

Preliminary charge

CIS 15.4.5

See Notes

- 01/12/2004

Increase in preliminary charge

CIS 15.4.6

See Notes

- 01/12/2004

Manager's obligation to redeem

CIS 15.4.7

See Notes

- 01/12/2004

Payment on redemption

CIS 15.4.8

See Notes

- 01/12/2004

Redemption price parameters

CIS 15.4.9

See Notes

- 01/12/2004

Redemption charge

CIS 15.4.10

See Notes

- 01/12/2004

Control over maximum charges on issue and redemption

CIS 15.4.11

See Notes

- 01/12/2004

Exchange of units in umbrella schemes

CIS 15.4.12

See Notes

- 01/12/2004

Notification of prices to the trustee

CIS 15.4.13

See Notes

- 01/12/2004

Publication of prices

CIS 15.4.14

See Notes

- 01/04/2005

Manner of price publication

CIS 15.4.15

See Notes

- 01/04/2005

CIS 15.5

Issues and cancellations through the manager and in specie cancellations

- 01/12/2004

Application

Purpose

CIS 15.5.2

See Notes

- 01/12/2004

Issues and cancellations through the manager

CIS 15.5.3

See Notes

- 01/11/2002

In specie cancellation

CIS 15.5.4

See Notes

- 01/12/2004

CIS 15.6

SDRT provision

- 01/12/2004

Application

CIS 15.6.1

See Notes

- 01/12/2004

Purpose

CIS 15.6.2

See Notes

- 01/08/2002

SDRT provision

CIS 15.6.3

See Notes

- 01/12/2004

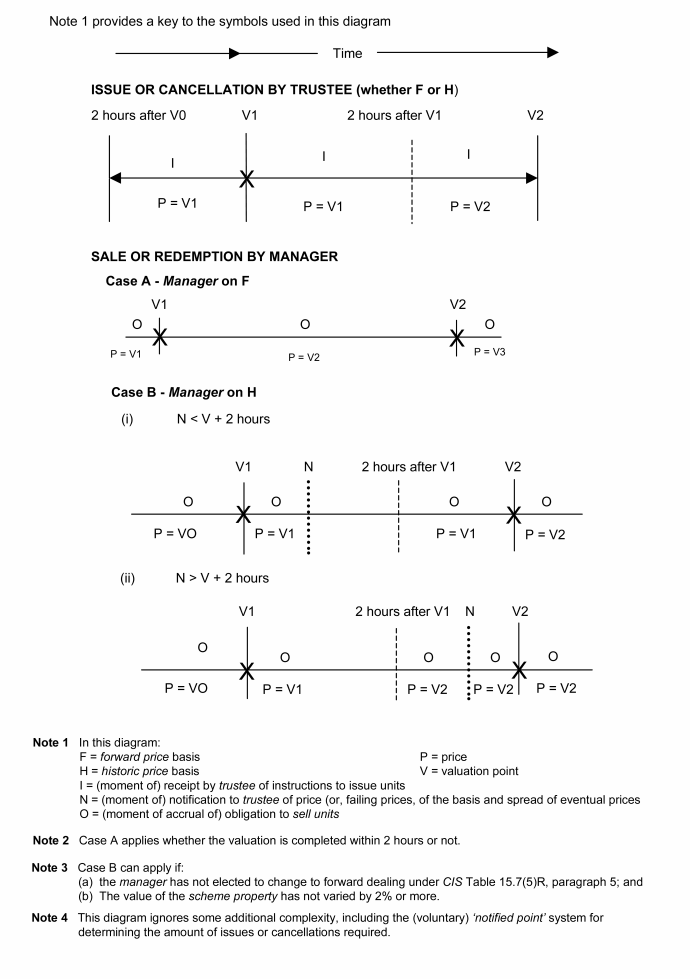

CIS 15.7

Forward and historic pricing

- 01/12/2004

Application

CIS 15.7.1

See Notes

- 01/12/2004

Purpose

CIS 15.7.2

See Notes

- 01/12/2004

CIS 15.7.3

See Notes

- 01/12/2004

Forward and historic pricing

CIS 15.7.4

See Notes

- 01/12/2004

CIS 15.7.5

See Notes

Explanatory table: Forward or historic pricing. This table belongs to CIS 15.7.4 R.

| FORWARD OR HISTORIC PRICING | |

| Part 1: General Dealing | |

| 1. | Manager's choice. The prospectus must state the manager's choice for H or else for F Only. |

| 2. | If the manager's current choice under 1 is F Only, all its deals must be at a forward price. |

| 3. | A manager must not choose H if its normal arrangements for valuation envisage valuations more than one business day apart. |

| 4. | The remainder of this table applies to a manager with a current choice of H. |

| 5. | It may at any time elect for F Only in respect of the rest of the then current dealing period. |

| 6. | If the manager binds itself to switch from H to F Only at a certain point in each dealing period, this must be stated in the prospectus. |

| 7. | An election for (or switch to) F Only will last until the end of the dealing period and will then lapse. |

| 8. | For general dealing purposes, redemptions must be on the same basis as sales. |

| Part 2: General Dealing - Duty To Adopt Forward Pricing | |

| 9. | Market movement: F Only applies once the manager having taken reasonable care decides that there would be a difference of 2% or more between the current value of the scheme property, if immediately valued, and its last calculated value (taking that as 100% for this purpose), but decides not to carry out an additional valuation under CIS 15.8.3 R (Valuation of scheme property). |

| 10. | Valuation taking over 2 hours: F Only applies if a new price for units of each class has not been notified to the trustee after 2 hours. |

| 11. | Paragraph (10) does not apply, if within two hours of the valuation point, the manager has notified the trustee of the basis (issue or cancellation) on which the next prices will be fixed, and of the spread (reckoned in percentage or money terms) between the maximum sale price and the minimum redemption price. |

| 12. | F Only under (9) and (10) will start when the relevant moment arrives, will last until the end of the dealing period and will then lapse. |

| Part 3: Individual Deviations | |

| 13. | Paragraphs (14) to (17) apply to an individual transaction without affecting the general position arrived at under Parts 1 and 2. |

| 14. | Request: F Only applies if the applicant for sale or redemption so requests. |

| 15. | Large deals: F Only applies, if the manager so decides, for a large deal. |

| 16. | Postal deals: F Only applies if the order or offer reaches the manager through the post or by any similar form of one-way communication. |

| 17. | Issue or cancellation through the manager: F Only applies in the case of an issue or cancellation under CIS 15.5.3 R (Issues and cancellations through the manager). |

| Part 4: Notification to Trustee | |

| 18. | The manager must notify the trustee of the fact and time of any adoption of F only under (5) or Part 2. |

- 01/12/2004

CIS 15.7.6

See Notes

- 01/12/2004

CIS 15.8

Valuation

- 01/12/2004

Application

CIS 15.8.1

See Notes

- 01/12/2004

Purpose

CIS 15.8.2

See Notes

- (1) This section protects investors by providing how the issue, cancellation, sale and redemption prices of units should be calculated. It also deals with the time and method of valuation of the scheme property, with the property that is to be included in a valuation and with the various tax and other adjustments that are either added to or deducted from such a valuation.

- (2) CIS 15.8.4 R contains the detailed rules for valuation of the scheme property by the manager. The Table is subject to other rules (see CIS 5.2.5 R (Valuation) or CIS 5A.2.5 R (Valuation) and CIS 12.3 (Property schemes)).

- 01/11/2002

Frequency of valuation

CIS 15.8.3

See Notes

- (1) Regular valuation: for the purposes of determining in accordance with these rules the prices at which units of either class may be issued, cancelled, sold or redeemed, the manager must regularly carry out a valuation of the scheme property, which must be conducted in accordance with CIS 15.8.4 R.

- (2) Additional valuation: the manager must inform the trustee if the manager determines to have an additional valuation point in respect of the AUT or any sub-fund, but this does not prevent the manager carrying out a valuation for another purpose that is not against the interests of the unitholders at a time that is not to be a valuation point.

- (3) An additional valuation must be conducted in accordance with CIS 15.8.4 R.

- (4) An additional valuation for the purposes of paragraph (9) (market movement) of CIS 15.7.5 R (forward and historic pricing) must be conducted:

- (a) in accordance with CIS 15.8.4 R; but

- (b) if it is impracticable to conduct a valuation in accordance with that table, the manager determines having taken reasonable care, and the trustee agrees, that an adequate valuation may be obtained in that way, may be conducted by reference to fluctuations in an index of property reflecting in the composition the scheme property the additional valuations may be conducted in that way.

- 01/12/2004

CIS 15.8.4

See Notes

Table 15.8R Valuation

This table belongs to CIS 15.8.3 R

| Section 1: When? | ||||

| 1. | The manager must carry out valuations under CIS 15.8.3 R (1) (Regular valuations) regularly. | |||

| 2. | The frequency of regular valuation must be specified in the prospectus. | |||

| 3. | The frequency specified must be at least twice a calendar month. | |||

| 4. | If the frequency specified is the minimum frequency, the regular valuations must be two weeks or more apart. | |||

| 5. | Paragraphs 3. and 4. do not apply to warrant schemes or to a sub-fund which is permitted to invest entirely in warrants and there must be at least one valuation point for them on each business day. | |||

| 6. | Additional valuations under CIS 15.8.3 R (2) can take place at any time during a dealing day. | |||

| 7. | There is no need to value during the period of an initial offer (but see CIS 15.2.6 R (Compulsory termination of initial offer)). | |||

| Section 2: How? | ||||

| 8. | The valuation takes place as at a valuation point fixed by the manager under Section 1. | |||

| 9. | The valuation is in base currency. | |||

| 10. | Prices must be the most recent prices that can reasonably be obtained after the valuation point with a view to giving an accurate valuation as at that point. | |||

| 11. | A valuation is in two parts, one on an issue basis and one on a cancellation basis. | |||

| 12. | To convert to base currency the value of property which would otherwise be valued in another currency the manager must either: | |||

| (a) | Select a rate of exchange which represents the average of the highest and lowest rates quoted at the relevant time for conversion of that currency into base currency on the market on which the manager would normally deal if it wished to make such a conversion; or | |||

| (b) | Invite the trustee to agree that it is in the interests of unitholders to select a different rate, and, if the trustee so agrees, use that other rate. | |||

| Section 3: What? | ||||

| 13. | All scheme property is included, subject to adjustments arising from this section, and section 4, and this section is to be applied as at the valuation point. | |||

| 14. | If the trustee has been instructed to issue or cancel units, assume (unless the contrary is shown) that: | |||

| (a) | it has done so; | |||

| (b) | it has paid or been paid for them; and | |||

| (c) | all consequential action required by these rules or by the trust deed has been taken. | |||

| 15. | If the trustee has issued or cancelled units but consequential action as at 14(c) is outstanding, assume that it has been taken. | |||

| 16. | If agreements for the unconditional sale or purchase of property are in existence but uncompleted, assume: | |||

| (a) | completion; and | |||

| (b) | that all consequential action required by their terms has been taken. | |||

| 17. | Do not include in 16. any agreement which is: | |||

| (a) | A future or contract for differences which is not yet due to be performed; or | |||

| (b) | An unexpired option written or purchased for the AUT which has not yet been exercised. | |||

| 18. | Include in 16 any agreement the existence of which is, or could reasonably be expected to be, known to the person valuing the property, assuming that all other persons in the manager's employment take all reasonable steps to inform it immediately of the making of any agreement. | |||

| Section 4: Tax and other adjustments | ||||

| 19. | Deduct an estimated amount for anticipated tax liabilities: | |||

| (a) | On unrealised capital gains where the liabilities have accrued and are payable out of the scheme property; | |||

| (b) | On realised capital gains in respect of previously completed and current accounting periods; | |||

| (c) | On income where the liabilities have accrued; | |||

| (d) | Including stamp duty reserve tax and any other fiscal charge not covered under this deduction. | |||

| 20. | Deduct: | |||

| (a) | an estimated amount for any liabilities payable out of the scheme property and any tax on it (treating any periodic items as accruing from day to day); | |||

| (b) | the principal amount of any outstanding borrowings whenever payable; | |||

| (c) | any accrued but unpaid interest on borrowings; | |||

| (d) | the value of any option written (if the premium for writing the option has become part of the scheme property); and | |||

| (e) | in the case of a margined contract, any amount reasonably anticipated to be paid by way of variation margin (that is the difference in price between the last settlement price, whether or not variation margin was then payable, and the price of the contract at the valuation point). | |||

| 21. | Add an estimated amount for accrued claims for repayment of taxation levied: | |||

| (a) | on capital (including capital gains); or | |||

| (b) | on income. | |||

| 22. | Add: | |||

| (a) | any other credit due to be paid into the scheme property; | |||

| (b) | in the case of a margined contract, any amount reasonably anticipated to be received by way of variation margin (that is the difference in price between the last settlement price, whether or not variation margin was then receivable, and the price of the contract at the valuation point); | |||

| (c) | any SDRT provision anticipated to be received. | |||

| Section 5: Issue Basis | ||||

| 23. | The valuation of property for that part of the valuation which is on a creation basis is as follows: | |||

| Property | To be valued at | |||

| (a) | Cash | nominal value | ||

| (b) | Amounts held in current and deposit accounts | nominal value | ||

| (c) | Property which is not within (a), (b) or (d): | |||

| (i) | if units in an AUT to which CIS 15 (Dual-pricing and dealing) applies | except where Note 1 applies, the most recent maximum sale price less any expected discount (plus dealing costs) [Note 2] | ||

| (ii) | if shares in an ICVC or units of an AUT to which CIS 4 (Single-pricing and dealing) applies | the most recent price (plus dealing costs) [Notes 2 and 3] | ||

| (iii) | if any other investment | best available market dealing offer price on the most appropriate market in a standard size (plus dealing costs) [Note 2] | ||

| (iv) | if other property, or no price exists under (i), (ii) or (iii). | manager's reasonable estimate of a buyer's price (plus dealing costs) [Notes 2 and 4] | ||

| (d) | Property which is a derivative under the terms of which there may be liability to make, for the account of the AUT, further payments (other than charges, and whether or not secured by margin) when the transaction in the derivative falls to be completed or upon its closing out. | |||

| (i) | if a written option under rule 20(d) | to be deducted (see 20(d)) at a net valuation of premium. [Notes 5 and 8] | ||

| (ii) | if an off-exchange future | net value on closing out [Notes 6 and 8] | ||

| (iii) | if any other such property | net value of margin of closing out (whether as a positive or negative figure) [Notes 7 and 8] | ||

| Notes | ||||

| 1. The issue price is taken, instead of the maximum sale price if the manager of the AUT whose scheme property is being valued is also the manager, or an associate of the manager, of the AUT whose units form part of that property. | ||||

| 2. In this Section and in Section 6, "dealing costs" means any fiscal charges, commission or other charges payable in the event of the AUT carrying out the transaction in question, assuming that the commission and charges (other than fiscal charges) which would be payable by the AUT are the least that could reasonably be expected to be paid in order to carry out the transaction. On the issue basis, dealing costs exclude any preliminary charge on sale of units in an AUT. | ||||

| 3. Dealing costs under note 2. Include any dilution levy or SDRT provision which would be added in the event of a purchase by the AUT of the units in question but, if the manager of the AUT being valued, or an associate of the manager, is also the manager of the AUT or the ACD of the ICVC whose units are held by the AUT, must not include a preliminary charge which would be payable in the event of a purchase by the AUT of those units. | ||||

| 4 The buyer's price is the consideration which would be paid by a buyer for an immediate transfer or assignment (or, in Scotland, assignation) to him at arm's length. | ||||

| 5. Estimate the premium on writing an option of the same series on the best terms then available on the most appropriate market on which such options are traded; but deduct dealing costs. | ||||

| 6. Estimate the amount of profit or loss receivable or incurable by the AUT on closing out the contract. Deduct minimum dealing costs in the case of profit and add them in the case of loss. | ||||

| 7. Estimate the amount of margin (whether receivable or payable by the AUT on closing out the contract) on the best terms then available on the most appropriate market on which such contracts are traded. If that amount is receivable (for example, the contract is "in the money") deduct minimum dealing costs. If, however, that amount is payable (for example, the contract is "out of the money") then add minimum dealing costs to the margin and the value is that figure as a negative sum. | ||||

| 8. If the property is an OTC transaction in derivatives, use the relevant valuation referred to in CIS 5.2.25 R (OTC transactions in derivatives) or CIS 5A.6.6 R (OTC transactions in derivatives). | ||||

| Section 6: Cancellation basis | ||||

| 24. | The valuation of property for that part of the valuation which is on a cancellation basis is as follows: | |||

| Property | To be valued at | |||

| (a) | Cash | nominal value | ||

| (b) | Amounts held in current deposit and loan accounts | nominal value | ||

| (c) | Property which is not within (a), (b) or (d): | |||

| (i) | if units in and AUT to which CIS 15 (Dual-pricing and dealing) applies | except where Note 1 applies, the most recent minimum redemption price (less dealing costs) [Note 2] | ||

| (ii) | if shares in an ICVC or units in an AUT to which CIS 4 (Single-pricing and dealing) applies | |||

| the most recent price (less dealing costs) [Notes 2 and 3] | ||||

| (iii) | if any other investment | best available market dealing bid price on the most appropriate market in a standard size (less dealing costs) [Note 2] | ||

| (iv) | if other property, or no price exists under (i) or (ii) | manager's reasonable estimate of a seller's price (less dealing costs) [Notes 2 and 4] | ||

| (d) | Property of the type described in 23.: | |||

| (i) | if a written option under 20.(d) | to be deducted (see 20(d)) at a net valuation of premium [Notes 5 and 8] | ||

| (ii) | if an off-exchange future | net value of closing out [Note 8] | ||

| (iii) | if any other such property | net value of margin on closing out (whether as a positive or negative figure) [Notes 6 and 8] | ||

| Notes | ||||

| 1. The cancellation price is taken instead of the minimum redemption price if the property, if sold in one transaction, would amount to a large deal. | ||||

| 2. For dealing costs see note 2. In 23.. Dealing costs include any charge payable on redemption of units in an AUT (taking account of any expected discount), except where the manager of the AUT whose property is being valued is also the manager, or an associate of the manager, of the AUT whose units form part of that property. | ||||

| 3. Dealing costs under note 2. include any dilution levy or SDRT provision which would be deducted in the event of a sale by the AUT of the units in question and, except when the manager of the AUT being valued, or an associate of the manager, is also the manager of the AUT or the ACD of the ICVC whose units are held by the AUT, include any charge payable on the redemption of those units (taking account of any expected discount). | ||||

| 4. The seller's price is the consideration which would be received by a seller for an immediate transfer or assignment (or, in Scotland, assignation) from him at arm's length, less dealing costs. | ||||

| 5. Estimate the premium on writing an option of the same series on the best terms then available on the most appropriate market on which such options are traded, and add dealing costs. | ||||

| 6. For off-exchange futures, see note 6 in 23. | ||||

| 7. For net value of margin see note 7 in 23. | ||||

| 8. For over the counter transactions in derivatives, see note 8 in 23. | ||||

- 01/11/2002

Valuation under SETS

CIS 15.8.5

See Notes

- (1) CIS 15.8.4 R requires certain property to be valued at the best available market dealing offer or bid price (depending on whether the property is being valued on an issue or cancellation basis) for a deal of standard size on the most appropriate market, after taking account of dealing costs. If no price exists, the manager is required to use a reasonable estimate of a buying or selling price.

- (2) Under the Stock Exchange Automated Quotation (SEAQ) System, the best market dealing offer or bid price in a particular security is generally understood to be the "touch" price. Under SETS, the London Stock Exchange publishes an "official best price" for each security, derived from the best prices displayed on the order book. It also publishes a "last trade price". The best bid price is the price of the highest buy order on the order book at any given time, and the best offer price is the price of the lowest sell order on the book. The last trade price for securities traded on SETS is published throughout the day. The "official closing price" is based on the last automatically executed trade taken from the order book.

- (3) A manager may wish to use the last trade price as the basis for valuing SETS securities held as part of the scheme property. The last trade price will be a precise figure, not an estimate, and there will be complete certainty that the security in question has traded at that price. Alternatively, a manager may use the best bid and offer price displayed on the order book as the basis of valuation. Either method is acceptable, provided that the manager documents the choice of method and ensures that the procedures are applied consistently and fairly. The basis on which the scheme property is to be valued must be set out in the AUT's prospectus, as required by CIS 3.5.2 R(17) (Valuation of scheme property).

- (4) Circumstances may arise where the chosen method may not provide a reliable basis for valuation. Guidance on such instances is provided at CIS 4.8.4 G(4) - (8). Additionally, where the manager imputes a 'spread' in order to arrive at an estimated buying or selling price - for example, in circumstances where there are no buy or sell orders on the order book, it should be able to justify any assumptions made.

- 01/04/2004